Concept explainers

Videos

Accounting for the Use and Disposal of Long-Lived Assets

Nicole’s Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $7,000. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 13,000 hours. Expected annual production was year 1, 3,100 hours; year 2, 2,500 hours; year 3, 3,400 hours; year 4, 2,200 hours; and year 5, 1,800 hours.

Required:

- 1. Complete a depreciation schedule for each of the alternative methods.

- a. Straight-line.

- b. Units-of-production.

- c. Double-declining-balance.

- 2. Assume NGS sold the hydrotherapy tub system for $2,100 at the end of year 3. Prepare the

journal entry to account for the disposal of this asset under the three different methods. - 3. The following amounts were

forecast for year 3: Sales Revenues $42,000; Cost of Goods Sold $33,000; Other Operating Expenses $4,000; and Interest Expense $800. Create an income statement for year 3 for each of the different depreciation methods, ending at Income before Income Tax Expense. (Don’t forget to include a loss or gain on disposal for each method.)

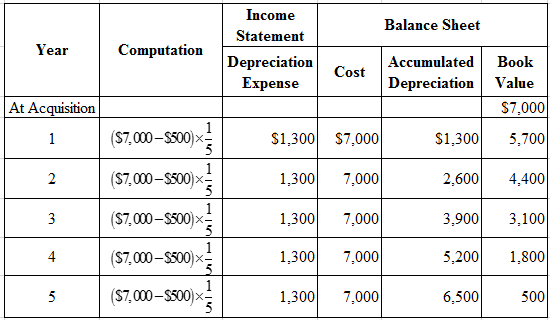

(1) (a)

Prepare the depreciation expense schedule under straight-line method

Explanation of Solution

Straight-line method: The depreciation method which assumes that the consumption of economic benefits of long-term asset could be distributed equally throughout the useful life of the asset is referred to as straight-line method.

Formula for straight-line depreciation method:

Depreciation expense: Depreciation expense is a non-cash expense, which is recorded on the income statement reflecting the consumption of economic benefits of long-term asset.

Accumulated depreciation: The total amount of depreciation expense deducted, from the time asset acquired till date, as reported in the account as on a particular date, is referred to as accumulated depreciation.

Formula for accumulated depreciation:

Book value: The amount of acquisition cost of less accumulated depreciation as on a particular date is referred to as book value.

Formula for book value:

Depreciation schedule under straight-line method:

Figure (1)

(1) (b)

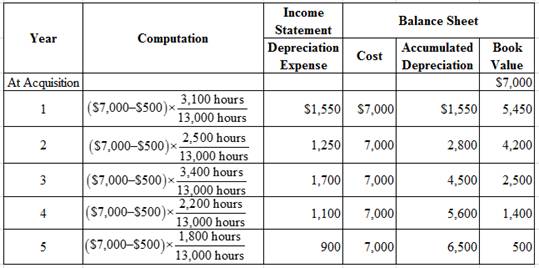

Prepare the depreciation expense schedule under units-of-production

Explanation of Solution

Units-of-production method: The depreciation method which assumes that the consumption of economic benefits of long-term asset is based on the production capacity or output is referred to as units-of-production method.

Formula for units-of-production depreciation method:

Depreciation schedule under units-of-production method:

Figure (2)

(1) (c)

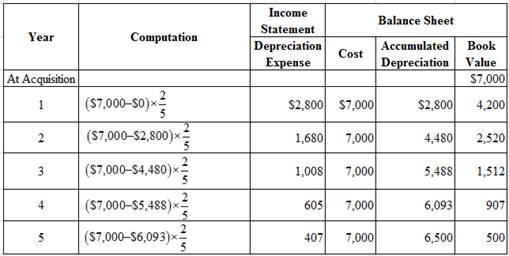

Prepare the depreciation expense schedule under double-declining-balance method

Explanation of Solution

Double-declining-balance method: The depreciation method which assumes that the consumption of economic benefits of long-term asset is high in the early years but gradually declines towards the end of its useful life, is referred to as double-declining-balance method.

Formula for double-declining-balance depreciation method:

Depreciation schedule under double-declining-balance method:

Figure (3)

Note:

Compute depreciation expense in Year 5.

(2)

Prepare the journal entries for the sale of equipment under three methods

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the sale of building, under straight-line method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 3,900 | |||||

| Loss on Disposal | 1,000 | |||||

| Equipment | 7,000 | |||||

| (To record sale of equipment) | ||||||

Table (1)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Building is a contra-asset account. Since the building is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Loss on Disposal is an expense account. Since losses and expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Building is an asset account. Since building is sold, asset account decreased, and a decrease in asset is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

Prepare journal entry for the sale of building, under units-of-production method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 4,500 | |||||

| Loss on Disposal | 400 | |||||

| Equipment | 7,000 | |||||

| (To record sale of equipment) | ||||||

Table (2)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Building is a contra-asset account. Since the building is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Loss on Disposal is an expense account. Since losses and expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Building is an asset account. Since building is sold, asset account decreased, and a decrease in asset is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

Prepare journal entry for the sale of equipment, under double-declining-balance method.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| Cash | 2,100 | |||||

| Accumulated Depreciation | 5,488 | |||||

| Equipment | 7,000 | |||||

| Gain on Disposal | 588 | |||||

| (To record sale of truck) | ||||||

Table (3)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accumulated Depreciation–Equipment is a contra-asset account. Since the equipment is sold, the accumulated depreciation balance is reversed to reduce the balance in the account; hence, the account is debited.

- Equipment is an asset account. Since equipment is sold, asset account decreased, and a decrease in asset is credited.

- Gain on Disposal is a revenue account. Since gains and revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Determine the gain on sale.

Step 1: Compute book value on the date of sale.

Step 2: Compute gain (loss) on sale.

(3)

Prepare the income statement of NG Spa for the Year 3, under three depreciation methods

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement for NG Spa for the Year 3.

| NG Spa | |||

| Income Statement | |||

| For Year 3 | |||

| Particulars | Straight-Line | Units-of-Production | Double-Declining-Balance |

| Sales revenue | $42,000 | $42,000 | $42,000 |

| Cost of goods sold | 33,000 | 33,000 | 33,000 |

| Gross profit | 9,000 | 9,000 | 9,000 |

| Operating expenses: | |||

| Depreciation expense | $1,300 | $1,700 | $1,008 |

| Other operating expenses | 4,000 | 4,000 | 4,000 |

| Loss (Gain) on disposal | 1,000 | 400 | (588) |

| Total operating expenses | 6,300 | 6,100 | 4,420 |

| Income from operations | 2,700 | 2,900 | 4,580 |

| Interest expense | 800 | 800 | 800 |

| Income before income tax expense | $1,900 | $2,100 | $3,780 |

Table (4)

Want to see more full solutions like this?

Chapter 9 Solutions

Fundamentals Of Financial Accounting

- IMPACT OF IMPROVEMENTS AND REPLACEMENTS ON THE CALCULATION OF DEPRECIATION On January 1, 20-1, two flight simulators were purchased by a space camp for 77,000 each with a salvage value of 5,000 each and estimated useful lives of eight years. On January 1, 20-2, the hydraulic system for Simulator A was replaced for 6,000 cash and an updated computer for more advanced students was installed in Simulator B for 9,000 cash. The hydraulic system is expected to extend the life of Simulator A three years beyond the original estimate. REQUIRED 1. Using the straight-line method, prepare general journal entries for depreciation on December 31, 20-1, for Simulators A and B. 2. Enter the transactions for January 20-2 in a general journal. 3. Assuming no other additions, improvements, or replacements, calculate the depreciation expense for each simulator for 20-2 through 20-8.arrow_forwardDuring the current year, Arkells Inc. made the following expenditures relating to plant machinery. Renovated five machines for $100,000 to improve efficiency in production of their remaining useful life of five years Low-cost repairs throughout the year totaled $70,000 Replaced a broken gear on a machine for $10,000 A. What amount should be expensed during the period? B. What amount should be capitalized during the period?arrow_forwardRequired information [The following information applies to the questions displayed below.) Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $8.500. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,250 hours; year 2, 2,350 hours; year 3, 2,300 hours, year 4, 2,100 hours; and year 5, 1,000 hours. 3. Assume NGS sold the hydrotherapy tub system for $2.550 at the end of year 3. The following amounts were forecast for year 3: Sales Revenues $44,000; Cost of Goods Sold $34,000; Other Operating Expenses $4,400, and Interest Expense $900. Create an income statement for year 3 for each of the different depreciation methods, ending at Income before Income Tax Expense. (Don't forget to include a loss or gain on disposal for each method.).…arrow_forward

- Required information [The following information applies to the questions displayed below. Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $8,500. The estimated useful life was five years and the residual value was $500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,250 hours: year 2, 2,350 hours; year 3, 2,300 hours: year 4, 2.100 hours; and year 5, 1,000 hours. Required: 1. Complete a depreciation schedule for each of the alternative methods. a. Straight-line. b. Units-of-production.. c. Double-declining-balance.arrow_forwardUniversity Car Wash purchased new soap dispensing equipment that cost $249,000 including installation. The company estimates that the equipment will have a residual value of $25,500. University Car Wash also estimates it will use the machine for six years or about 12,500 total hours. Actual use per year was as follows: Year 1 2 3 4 5 6 Total Year 1 2 3 4 5 6 Problem 7-5A (Algo) Part 3 3. Prepare a depreciation schedule for six years using the activity-based method. (Round your "Depreciation Rate" to 2 decimal places and use this amount in all subsequent calculations.) Hours Used 2,900 1,800 1,900 2,100 1,900 1,900 $ UNIVERSITY CAR WASH Depreciation Schedule-Activity-Based End of Year Amounts Depreciation Expense 0 Accumulated Depreciation Book Valuearrow_forwardClean Air Company makes and sells cloth masks. The company purchased a new automated sewing machine at the beginning of Year 1 for $87,000. The machine is expected to have a two-year useful life and a $21,700 salvage value. The expected mask production is estimated at 130,600 masks. Actual mask production for the two years was as follows: Year 1 Year 2 Total Required: 72,000 65,000 137,000 Compute the depreciation expense for each of the two years, using units-of-production depreciation. Year 1 Year 2 Depreciation expense Charrow_forward

- applies to the questions displayed below.] Nicole's Getaway Spa (NGS) purchased a hydrotherapy tub system to add to the wellness programs at NGS. The machine was purchased at the beginning of the year at a cost of $15,500. The estimated useful life was five years and the residual value was $1,500. Assume that the estimated productive life of the machine is 10,000 hours. Expected annual production was year 1, 2,350 hours; year 2, 2,500 hours; year 3, 2,050 hours; year 4, 2,100 hours; and year 5, 1,000 hours. 3. Assume NGS sold the hydrotherapy tub system for $4,650 at the end of year 3. The following amounts were forecast for year 3: Sales Revenues $52,000; Cost of Goods Sold $41,000; Other Operating Expenses $4,500; and Interest Expense $700. Create an income statement for year 3 for each of the different depreciation methods, ending at Income before Income Tax Expense. (Don't forget to include a loss or gain on disposal for each method.). (Do not round intermediate calculations. Round…arrow_forwardA high-precision programmable router for shaping furniture components is purchased by Henredon for $190,000. It is expected to last 12 years. Calculate the depreciation deduction and book value for each year using MACRS-GDS allowances. a. What is the MACRS-GDS property class? b. Assume the complete allowable depreciation schedule is used. c. Assume the asset is sold during the 5th year of use.arrow_forwardUniversity Car Wash purchased new soap dispensing equipment that cost $234,000 including installation. The company estimates that the equipment will have a residual value of $27,000. University Car Wash also estimates it will use the machine for six years or about 12,000 total hours. Actual use per year was as follows: Year Hours Used 1 2,800 2 1,900 3 2,000 4 2,000 5 1,800 6 1,500 3. Prepare a depreciation schedule for six years using the activity-based method. (Round your "Depreciation Rate" to 2 decimal places and use this amount in all subsequent calculations.)arrow_forward

- A high-precision programmable router for shaping office furniture components (office furniture manufacturing equipment) is purchased by Henredon for $350,000. It is expected to last 12 years. Calculate the depreciation deduction and book value for each year using MACRS-GDS allowances. a. What is the MACRS-GDS property class? Provide your answer in year (format example: 3 year) Calculate the depreciation deduction using MACRS- GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.) Calculate the book value using MACRS-GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.) Assume the asset is sold during the 5th year of use. Calculate the depreciation deduction using MACRS-GDS allowances for year 5 = $. (Please provide your response to the nearest integer with no comma or $ sign.)arrow_forwardAn injection molding machine can be purchased and installed for $90,000. It is in the seven-year GDS property class and is expected to be kept in service for eight years. It is believed that $11,000 can be obtained when the machine is disposed of at the end of year eight. The net annual value added (i.e., revenues less expenses) that can be attributed to this machine is constant over eight years and amounts to $19,000. An effective income tax rate of 45% is used by the company, and the after-tax MARR equals 18% per year. Click the icon to view the GDS Recovery Rates (r) for the 7-year property class. a. What is the approximate value of the company's before-tax MARR? The before-tax MARR is %. (Round to the nearest whole number.) b. Determine the GDS depreciation amounts in years one through eight. (Round to the nearest dollar.) IT Year Depreciation, $ 1 4 5 6 8 c. What is the taxable income at the end of year eight that is related to capital investment? The taxable income at the end of…arrow_forwardcommunity hospital in a rual community operates the ambulance service. the hospital purchases a new ambulance for $150,000. they estimate a useful life of 10 years and a salvage value of $20,000. what is the annual charge for depreciation on this asset?arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT