Concept explainers

Videos

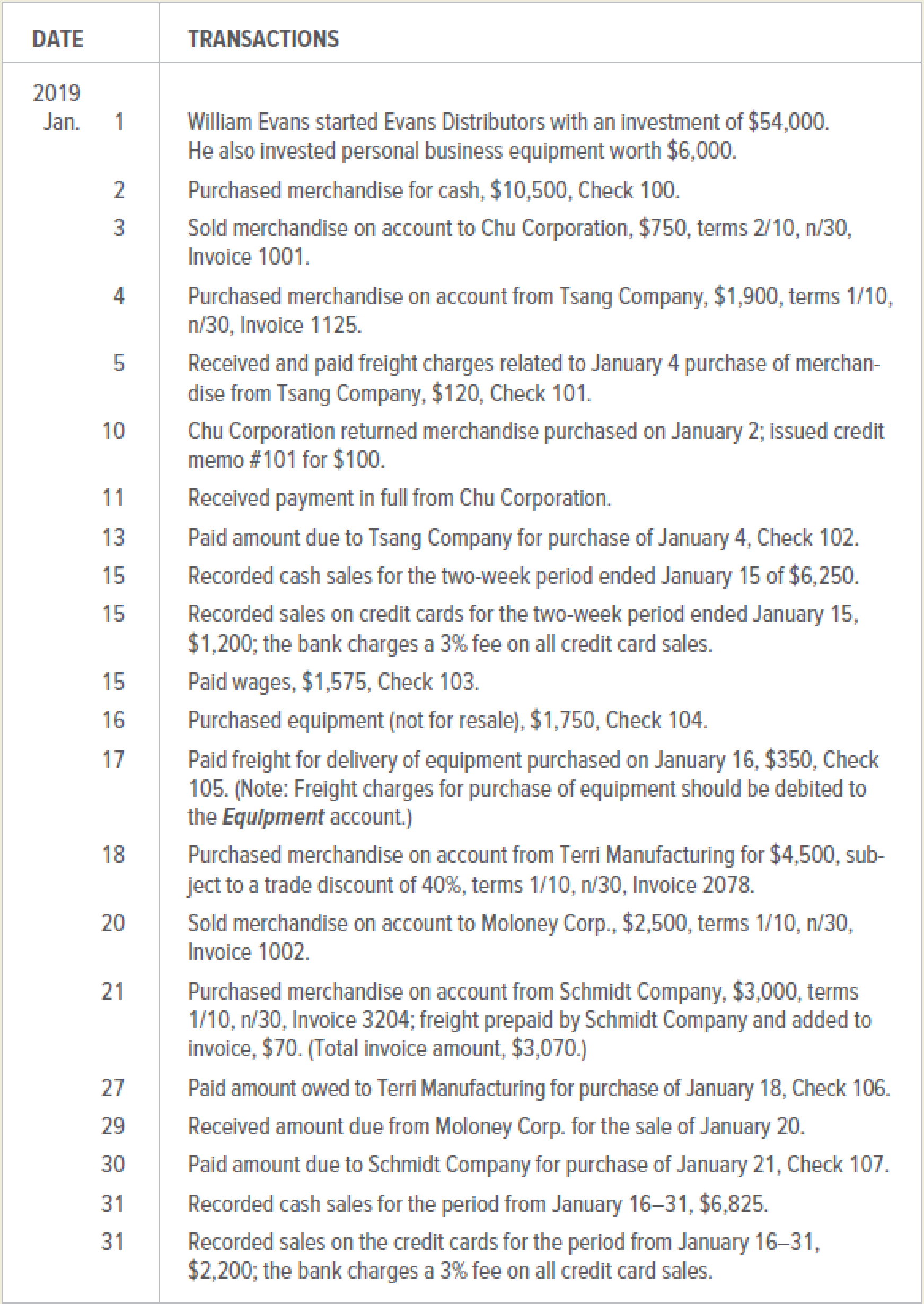

William Evans began Evans Distributors, a sporting goods distribution company, in January 2019 and engaged in the transactions below. Assume Evans Distributors and its customers take advantage of all cash discounts.

INSTRUCTIONS

Record the transactions in a general journal. Number the first journal as page 1. Provide brief explanations after each

Prepare general journal for the transactions of company ED.

Explanation of Solution

General Journal:

All the transactions of a business are prima facie recorded in general journal in chronological order. The general ledger is also known as the primary books of account.

Record the transactions in the general journal as follows:

Recording the capital invested:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 1, 2019 | Cash | 54,000 | ||

| Equipment | 6,000 | |||

| Capital | 60,000 | |||

| (to record the capital invested and equipment provided) | ||||

Table (1)

- • The cash account is an asset account and the account balance is increasing. Therefore, it is debited.

- • The equipment account is asset account and the balance of account is increasing. Therefore, it is debited.

- • The capital account is owners’ equity account. The balance is increased by introducing capital. Hence, it is credited.

Recording the merchandise purchased on cash:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 2, 2019 | Purchases | 10,500 | ||

| Cash | 10,500 | |||

| (to record the merchandise purchased for cash) | ||||

Table (2)

- • The purchases account is expense account and has a normal debit balance which is increasing. Hence, it is debited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the merchandise sold on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 3, 2019 | Accounts receivables/Company C | 750 | ||

| Sales | 750 | |||

| (to record the merchandise sold on account with terms 2/10, n/30) | ||||

Table (3)

- • The accounts receivable is an asset and the account balance is increasing. Hence, it is debited.

- • The sales account is a revenue account. The revenue is generated on selling the merchandise. Hence, it is credited.

Recording the merchandise purchased on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 4, 2019 | Purchases | 1,900 | ||

| Accounts payable/Company TS | 1,900 | |||

| (to record the merchandise purchased on account with terms 1/10, n/30) | ||||

Table (4)

- • The purchases account is expense account and has a normal debit balance which is increasing. Hence, it is debited.

- • Accounts payable is a liability and the account balance is increasing. Therefore, it is credited.

Recording the freight charges paid:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 5, 2019 | Freight In | 120 | ||

| Cash | 120 | |||

| (to record the freight charges paid) | ||||

Table (5)

- • Freight-in charges are the expenses and the expenses are increasing. Hence, the account is debited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the sold goods returned:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 10, 2019 | Sales returns and allowances | 100 | ||

| Accounts receivables/Company C | 100 | |||

| (to record goods returned and credit memo issued) | ||||

Table (6)

- • The sales returns and allowances account is identified as contra revenue account with normal debit balance and increasing. Therefore, it is debited.

- • The account receivable account is an asset account and the account balance is decreasing. Therefore, the accounts payable account is credited.

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 11, 2019 | Sales Discount | 13 | ||

| Cash | 637 | |||

| Accounts receivable/Company C | 650 | |||

| (to record the payment received and discount provided) | ||||

Table (7)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is an asset account and the account balance is increasing. Therefore, it is debited.

- • The accounts receivable account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 13, 2019 | Accounts payable/Company TS | 1,900 | ||

| Purchases discounts | 19 | |||

| Cash | 1,881 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (8)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on cash:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 15, 2019 | Purchases | 6,250 | ||

| Cash | 6,250 | |||

| (to record the inventory purchased on cash) | ||||

Table (9)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold using credit card:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 15, 2019 | Credit card expense | 36 | ||

| Cash | 1,164 | |||

| Sales | 1,200 | |||

| (to record the merchandise sold on) | ||||

Table (10)

- • The credit card expense is the expense account which has normal debit balance. The balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and the account balance is increasing. Therefore, the cash account is debited.

- • The sales account is identified as the revenue account and the revenue is generated from selling merchandise. Therefore, sales account is credited.

Recording the wages paid:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 15, 2019 | Wages | 1,575 | ||

| Cash | 1,575 | |||

| (to record the wages paid) | ||||

Table (11)

- • Wages are the expenses and the expenses are increasing. Hence, it is debited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchase of equipment:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 16, 2019 | Equipment | 1,750 | ||

| Cash | 1,750 | |||

| (to record the equipment purchased) | ||||

Table (12)

- • Equipment is an asset and the account balance of asset is increasing. Hence, the account is debited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the charges paid for transporting equipment:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 17, 2019 | Equipment | 350 | ||

| Cash | 350 | |||

| (to record the freight charges paid on equipment) | ||||

Table (13)

- • Freight-in charges are the expenses and the expenses are increasing. Hence, the account is debited. The freight-in charges related to transport of equipment are debited to the equipment account only.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 18 , 2019 | Purchases | 1,700 | ||

| Accounts payable/Company TE | 1,700 | |||

| (to record the inventory purchased on account with terms1/10, n/30) | ||||

Table (14)

- • The purchases account is debited. This is because the purchase account is an expense account and has normal debit balance which is increasing.

- • Accounts payable is liability and account balance is increasing. Therefore, it is credited.

Recording the merchandise sold on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 20, 2019 | Accounts receivables/Company M | 2,500 | ||

| Sales | 2,500 | |||

| (to record the merchandise sold on account with terms 1/10, n/30) | ||||

Table (15)

- • The accounts receivable is an asset and the account balance is increasing. Hence, it is debited.

- • The sales account is a revenue account. The revenue is generated on selling the merchandise. Hence, it is credited.

Record the purchases on the credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 21, 2019 | Purchases | 3,000 | ||

| Freight In | 70 | |||

| Accounts payable/Company S | 3,070 | |||

| (to record the inventory purchased on account with terms 1/30, n/30) | ||||

Table (16)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Freight-in charges are the expenses and the expenses are increasing. Hence, the account is debited.

- • The accounts payable is a liability and the account balance is increasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 27, 2019 | Accounts payable/Company TE | 2,700 | ||

| Purchases discounts | 27 | |||

| Cash | 2,673 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (17)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 29, 2019 | Sales Discount | 25 | ||

| Cash | 2,475 | |||

| Accounts receivable/Company M | 2,500 | |||

| (to record the payment received and discount provided) | ||||

Table (18)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is asset account and the account balance is increasing. Hence, cash account is debited. The amount in cash account would be calculated by subtracting the merchandise returned by the buyer and the sales discount provided.

- • The accounts receivable account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 30, 2019 | Accounts payable/Company S | 3,070 | ||

| Purchases discounts | 30 | |||

| Cash | 3,040 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (19)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on cash:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 30, 2019 | Purchases | 6,825 | ||

| Cash | 6,825 | |||

| (to record the inventory purchased on cash) | ||||

Table (20)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold using credit card:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 30, 2019 | Credit card expense | 66 | ||

| Cash | 2,134 | |||

| Sales | 2,200 | |||

| (to record the merchandise sold on) | ||||

Table (21)

- • The credit card expense is the expense account which has normal debit balance. The balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and the account balance is increasing. Therefore, the cash account is debited.

- • The sales account is identified as the revenue account and the revenue is generated from selling merchandise. Therefore, sales account is credited.

Working Note:

Calculation for sales discount:

The sales discount is provided to the customer by the seller fulfilling the terms of making the timely payments as per 2/10, n/30 terms. The customer is entitled to receive the two percent of sales discount on the merchandise sold if the payment is made with ten days of invoice provided.

The amount calculated as per given information would be $13.

Calculation of purchases discount:

The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company TS was agreed as 1/10, n/30. The terms 1/10, n/30 means the buyer is entitled to receive one percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $19.

Calculations for the credit card expense:

The fee is charged for availing the services of credit card. The bank fee to be charged as credit card is given as three percent for all credit card sales.

The expense would amount to be $36.

Calculations for the purchases amount:

The seller provides the trade discount of forty percent on the list price to the buyer. The purchases amount to be recorded by the buyer would be at the invoice price.

The purchases amount that would be calculated is $2,700.

Calculation of purchases discount:

The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company TE was agreed as 1/10, n/30. The terms 1/10, n/30 means the buyer is entitled to receive one percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $27.

Calculation for sales discount:

The sales discount is provided to the customer by the seller fulfilling the terms of making the timely payments as per 1/10, n/30 terms. The customer is entitled to receive the one percent of sales discount on the merchandise sold if the payment is made with ten days of invoice provided.

The amount calculated as per given information would be $25.

Calculation of purchases discount:

The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company S was agreed as 1/10, n/30. The terms 1/10, n/30 means the buyer is entitled to receive one percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $30.

Calculations for the credit card expense:

The fee is charged for availing the services of credit card. The bank fee to be charged as credit card is given as three percent for all credit card sales.

The expense would amount to be $66.

Want to see more full solutions like this?

Chapter 8 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

- Blue Company, an architectural firm, has a bookkeeper who maintains a cash receipts and disbursements journal. At the end of the year (2019), the company hires you to convert the cash receipts and disbursements into accrual basis revenues and expenses. The total cash receipts are summarized as follows. The accounts receivable from customers at the end of the year are 120,000. You note that the accounts receivable at the beginning of the year were 190,000. The cash sales included 30,000 of prepayments for services to be provided over the period January 1, 2019, through December 31, 2021. a. Compute the companys accrual basis gross income for 2019. b. Would you recommend that Blue use the cash method or the accrual method? Why? c. The company does not maintain an allowance for uncollectible accounts. Would you recommend that such an allowance be established for tax purposes? Explain.arrow_forwardThe following selected accounts and their current balances appear in the ledger of Clairemont Co. for the fiscal year ended May 31, 2019: Instructions 1. Prepare a multiple-step income statement. 2. Prepare a statement of owners equity. 3. Prepare a balance sheet, assuming that the current portion of the note payable is 50,000. 4. Briefly explain how multiple-step and single-step income statements differ.arrow_forwardTransactions related to purchases and cash payments completed by Wisk Away Cleaning Services Inc. during the month of May 20Y5 are as follows: Prepare a purchases journal and a cash payments journal to record these transactions. The forms of the journals are similar to those illustrated in the text. Place a check mark () in the Post. Ref. column to indicate when the accounts payable subsidiary ledger should be posted. Wisk Away Cleaning Services Inc. uses the following accounts:arrow_forward

- Record in journal form the following transaction: Bought goods on credit for $4,500 from Andrew 23 December 2019, terms 10/10, n/30. Paid for them 31 December 2019.arrow_forwardThe following transactions relating to an enterprise. Prepare sales, purchases, returns outward day books. 2019 May 1 Credit sales: T Thompson OMR 56; L Rodriguez OMR 148; K Barton OMR 145. 3 Credit purchases: P Potter OMR 144; H Harris OMR 25; B Spencer OMR 76. 7 Credit sales: K Kelly OMR 89; N Mendes OMR 78; N Lee OMR 257. 9 Credit purchases: B Perkins OMR 24; H Harris OMR 58; H Miles OMR 123. 11 Goods returned by us to: P Potter OMR 12; B Spencer OMR 22. 14 Goods returned to us by: T Thompson OMR 5; K Barton OMR 11; K Kelly OMR 14. 17 Credit purchases: H Harris OMR 54; B Perkins OMR 65; L Nixon OMR 75. 20 Goods returned by us to B Spencer OMR 14. 24 Credit sales: K Mohammed OMR 57; K Kelly OMR 65; O Green OMR 112. 28 Goods returned to us by N Mendes OMR 24. 31 Credit sales: N Lee OMR 55.arrow_forwardThe cash payments and purchases journals for Bill's Landscaping Co. are shown below. The accounts payable control account has an April 1, 2019, balance of $6,986, consisting of an amount owed to Augusta Sod Co. CASH PAYMENTS JOURNAL Page 38 Other Accounts Ck. Post. Accounts Payable Cash Date No. Account Debited Ref. Dr. Dr. Cr. 2019 Apr. 4 106 Augusta Sod Co. 107 Utilities Expense 6,986 6,986 Apr. 5 54 642 642 Apr. 15 108 Kimble Lumber Co. 3,644 3,644 2,872 13,502 Apr. 27 109 Schott's Fertilizer 2,872 Apr. 30 642 14,144 (V) (21) (11) PURCHASES JOURNAL Page 22 Landscaping Supplies Accounts Other Post. Payable Accounts Post. Date Account Debited Ref. Cr. Dr. Dr. Ref. Amount 2019 Apr. 3 Kimble Lumber Co. 3,644 3,644 7,807 Apr. 5 Apr. 14 Cooke Equipment Co. Equipment 18 7,807 Schott's Fertilizer 2,872 2,872 Apr. 24 Augusta Sod Co. 4,251 4,251 Apr. 29 Kimble Lumber Co. 9,091 9,091 Apr. 30 27,665 19,858 7,807 (21) (14) (V) Prepare the accounts payable subsidiary ledger, and determine that…arrow_forward

- Asset Cost: Less: Residual Value Depreciable Amount Depreciation method Depreciation p.a: Date 30/06/2018 30/06/2019 30/06/2020 Computers Depreciation Worksheet - Snow Lake Pty Ltd $66,000 $ N/A $66,000 Reducing Balance (Diminishing Balance) 30% Asset Cost $66,000 46,200 32,340 Depreciation $19,800 13,860 9,702 Accumulated Depreciation $19,800 33,660 43,362 Carrying Amount at the end $46,200 32,340 22,638 20 2014 2015 14200 1444arrow_forward1 . Prepare journal entries to record the following transactions entered into by Ivanhoe Company: (Credit account titles are automatically indented when the amount is entered. Do not indent manually. Record journal entries in the order presented in the problem. List all debit entries before credit entries.) 2020 June 1 Received a $8,600, 12%, 1-year note from Andrea Foley as full payment on her account. Nov. 1 Sold merchandise on account to Patton, Inc. for $10,320, terms 2/10, n/30. Nov. 5 Patton, Inc. returned merchandise worth $520 Nov. 9 Received payment in full from Patton, Inc. Dec. 31 Accrued interest on Foley's note. 2021 June 1 Andrea Foley honored her promissory note by sending the face amount plus interest. No interest has been accrued in 2021.arrow_forwardThe following selected transactions were completed by Zippy Do Co., a supplier of zippers for clothing: 2019 Dec. 1 2 2 3 4 5 6 7 8 0 9 10 11 12 12 13 14 15 16 17 3 2020 Mar. 2 Received payment of note and interest from Chicago Clothing & Bags Co. Journalize the entries to record the transactions. If no entry is required, simply skip to the next transaction. Be sure to include the year in the date for the entries. 18 19 20 31 31 Page 10 Accounting 1A Class Assignment Chapter 8-Receivables Received from Chicago Clothing & Bags Co., on account, a $36,000, 90-day, 6% note dated December 3. Recorded an adjusting entry for accrued interest on the note of December 3. Recorded the closing entry for interest revenue. Date GENERAL JOURNAL Description Post ref Debit Page Credit 1 2 3 4 5 6 0 7 191 8 9 10 11 12 13 14 15 16 17 18 19 20 Page <arrow_forward

- Read through the information below for selected transactions during the month of December, 2021 and prepare the required jounal entry to record the transaction. Post each of the entries below to the general ledger T-accounts attached . Sold Merchandise for $5,000 to Lee Corp on account on December 9. Cost of the merchandise was $3,390 and the terms of the sale were 1/15, n/30.arrow_forwardThe following selected accounts and their current balances appear in the ledger of Kanpur Co. for the fiscal year ended June 30, 2019: 1. Prepare a multiple-step income statement.2. Prepare a statement of owner’s equity.3. Prepare a balance sheet, assuming that the current portion of the note payable is$7,000.4. Briefly explain how multiple-step and single-step income statements differ.arrow_forwardLloyd Gurango Co. completed the following sales transactions during the month of June 2019. All credit sales have terms of 3/10, n/30 and all invoices are dates as at the transaction date. June 1 Sold merchandise on account to KRA Company, P32 000. Invoice number 377 Sold merchandise on account to LRM Trading, P54 000. Invoice number 378. Sold P46 000 of merchandise for cash. Received payment from KRA Company, less discounts. Received payment from LRM Trading, less discounts. Sold merchandise to JPT Store on account, P62 000. Invoice number 379. 6. Borrowed P30 000 from the Unlad Bank issuing a 10% note payable due in 3 JPT Store returned P11 000 of merchandise from the June 13 sale. Sold merchandise to NOV Convenience Store on account, P17 000. Invoice months number 380. Collected amount due from JPT Store less returns and discounts. 16 Received P6 000 from NOV Convenience Store. Sold goods on account to LPR Co, P34 000. Invoice number 381 347935arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning