Concept explainers

Videos

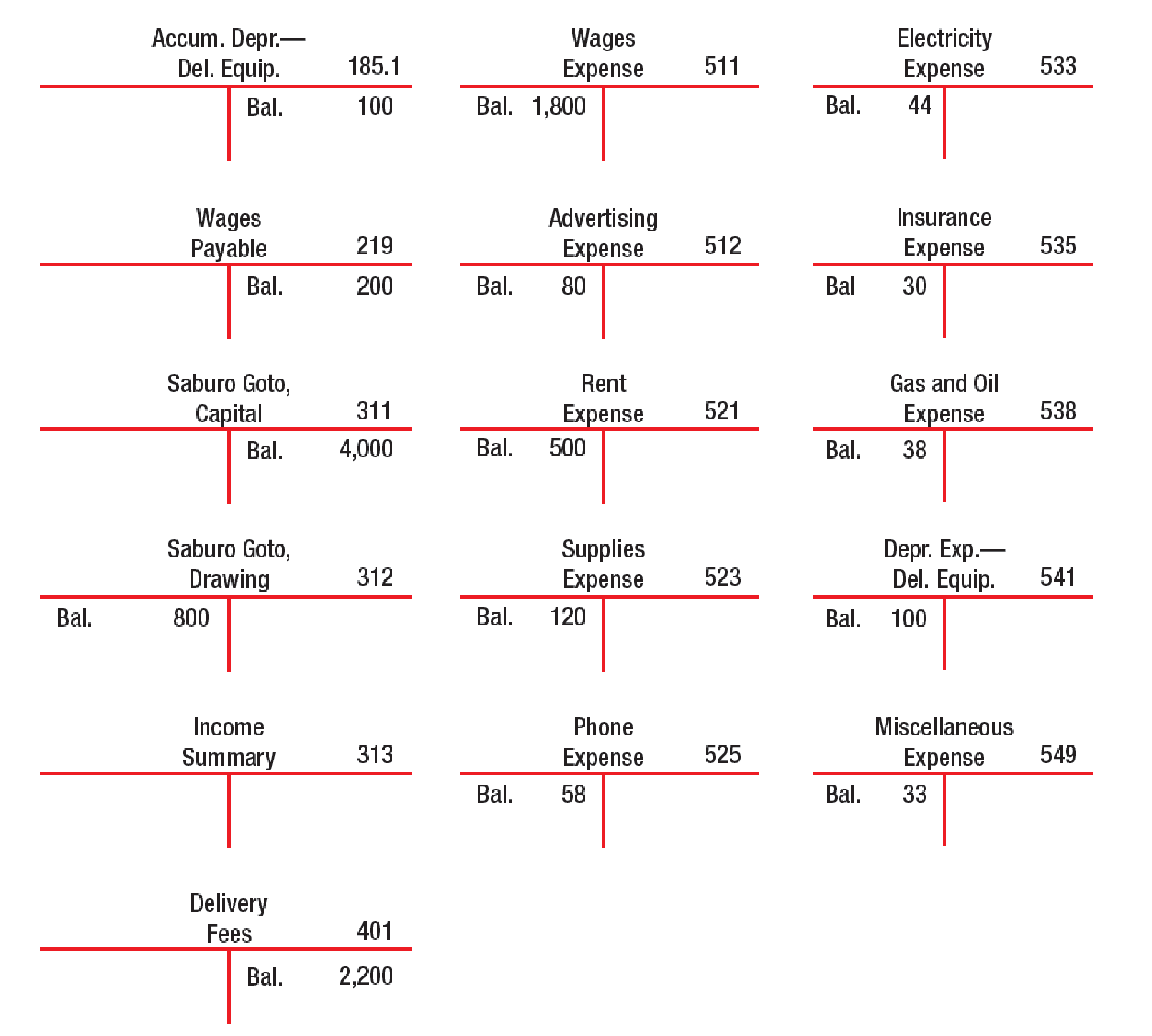

CLOSING ENTRIES (NET LOSS) Using the following partial listing of T accounts, prepare closing entries in general journal form dated January 31, 20--. Then

Prepare closing journal entries in general journal form and post those entries to the T accounts.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to permanent account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare the closing entries.

| Date | Accounts and Explanation |

Account Number |

Debit ($) | Credit ($) |

| June 30 | Referral fees (SE–) | 401 | 2,813 | |

| Income Summary (SE+) | 313 | 2,813 | ||

| (To close the revenue account.) | ||||

| June 30 | Income summary (SE–) | 313 | 2,987 | |

| Wages expense (SE+) | 511 | 1,080 | ||

| Advertising expense (SE+) | 512 | 34 | ||

| Rent expense (SE+) | 521 | 900 | ||

| Supplies expense (SE+) | 523 | 322 | ||

| Phone expense (SE+) | 525 | 133 | ||

| Utilities expense (SE+) | 533 | 102 | ||

| Insurance expense (SE+) | 535 | 120 | ||

| Gas and oil expense (SE+) | 538 | 88 | ||

| Depreciation expense (SE+) | 541 | 110 | ||

| Miscellaneous expense (SE+) | 549 | 98 | ||

| (To close the expense accounts.) | ||||

| June 30 | RZ, Capital (SE+) | 313 | 174 | |

| Income Summary (SE–) | 313 | 174 | ||

| (To close the income summary accounts) | ||||

| June 30 | RZ, Capital (SE–) | 311 | 2,000 | |

| RZ, Drawings (SE+) | 312 | 2,000 | ||

| (To close withdrawals account.) |

Table (1)

Working Note:

Calculate the amount of RZ capital (transferred).

Revenue account: In this closing entry, the referral fees account is closed by transferring the amount of referral fees account to Income summary account in order to bring the revenue account balance to zero. Hence, debit referral fees account and credit Income summary account.

Expense account: In this closing entry, all expense accounts are closed by transferring the amount of total expense to the Income summary account in order to bring the expense account balance to zero. Hence, debit the Income summary account and credit all expenses account.

Income summary account: Income summary account is a temporary account. This account is debited to close the net income value to RZ capital account.

RZ capital is a component of stockholders’ equity account. The value of RZ capital increased because net income is transferred. Therefore, it is credited.

Withdrawals account: RZ capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

RZ withdrawals are a component of owner’s equity. It is credited because the balance of owners’ withdrawals account is transferred to owners ‘capital account.

T-account: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

Posting the closing entries to the T- account:

| Accumulated Depreciation | Account No – 181.1 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Ending balance | 110 | Beginning balance | 110 | |||

| Beginning balance | 110 | |||||

Table (2)

| Wages Payable | Account No - 219 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Ending balance | 260 | Beginning balance | 260 | |||

| Beginning balance | 260 | |||||

Table (3)

| RZ Capital | Account No – 311 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Income summary | 174 | Beginning balance | 6,000 | |||

| RZ Drawings | 2,000 | |||||

| Ending balance | 3,826 | |||||

| Beginning balance | 3,826 | |||||

Table (4)

| SG Drawings | Account No - 312 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 2,000 | RZ Capital | 2,000 | |||

| Total | 2,000 | Total | 2,000 | |||

Table (5)

| Income Summary | Account No - 313 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Total expense | 2,987 | Referral fees | 2,813 | |||

| RZ Capital | 174 | |||||

| Total | 2,987 | Total | 2,987 | |||

Table (6)

| Referral Fees | Account No - 401 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Income summary | 2,813 | Beginning balance | 2,813 | |||

| Total | 2,813 | Total | 2,813 | |||

Table (7)

| Wages Expense | Account No - 511 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 1,080 | Income summary | 1,080 | |||

| Total | 1,080 | Total | 1,080 | |||

Table (8)

| Advertising Expense | Account No - 512 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 34 | Income summary | 34 | |||

| Total | 34 | Total | 34 | |||

Table (9)

| Rent Expense | Account No - 521 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 900 | Income summary | 900 | |||

| Total | 900 | Total | 900 | |||

Table (10)

| Supplies Expense | Account No - 524 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 322 | Income summary | 322 | |||

| Total | 322 | Total | 322 | |||

Table (11)

| Phone Expense | Account No - 525 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 133 | Income summary | 133 | |||

| Total | 133 | Total | 133 | |||

Table (12)

| Utilities Expense | Account No - 533 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 102 | Income summary | 102 | |||

| Total | 102 | Total | 102 | |||

Table (13)

| Insurance Expense | Account No - 535 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 120 | Income summary | 120 | |||

| Total | 120 | Total | 120 | |||

Table (14)

| Gas and Oil Expense | Account No - 538 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 88 | Income summary | 88 | |||

| Total | 88 | Total | 88 | |||

Table (15)

| Depreciation Expense | Account No - 541 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 110 | Income summary | 110 | |||

| Total | 110 | Total | 110 | |||

Table (16)

| Miscellaneous Expense | Account No - 549 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 98 | Income summary | 98 | |||

| Total | 98 | Total | 98 | |||

Table (17)

Want to see more full solutions like this?

Chapter 6 Solutions

College Accounting, Chapters 1-27 (New in Accounting from Heintz and Parry)

- Closing Entries (Net Income) Use the following partial listing of T accounts to complete this exercise. 1. Prepare closing entries dated April 30, 20--. Do not enter the posting references until you complete part 2. If an amount box does not require an entry, leave it blank. 2. Post the closing entries to the T accounts following the top-down journal entry order. If there is more than one closing entry for an account, enter in the order given in the journal above. Then, complete the posting for part 1. Cash 101 Bal. 500 Accounts Receivable 122 Bal. 1,500 Wages Payable 219 Bal. 400 Javian Davis, Capital 311 Bal. 9,000 Javian Davis, Drawing 312 Bal. 1,000 Income Summary 313 Tennis Instruction Fees 401 Bal. 4,000 Wages Expense 511 Bal. 760 Advertising Expense 512 Bal. 200 Travel Expense 515 Bal. 600 Supplies Expense 524 Bal. 500 Insurance Expense 535…arrow_forwardFind year-end closing entries (journal and ledger).arrow_forwardUse the May 31 fiscal year-end information from the following ledger accounts (assume that all accounts have normal balances) to prepare closing journal entries and then post those entries to ledger accounts.arrow_forward

- Use the filling partial listing of T accounts to complete this exercise. 1)Prepare closing entries in general journal form dates May 31,20– 2) post the closing entries to the T accounts.arrow_forward1. Prepare closing entries in general journal form dated May 31, 20--. Do not enter the posting references until you complete part 2. If an amount box does not require an entry, leave it blank. 2. Post the closing entries to the T accounts following the top-down journal entry order. If there is more than one closing entry for an account, enter in the order given in the journal . Then, complete the posting in part 1. Use the following partial listing of T accounts to complete this exercise. Cash 101 Bal. 600 Accounts Receivable 122 Bal. 1,800 Wages Payable 219 Bal. 500 Mark Thrasher, Capital 311 Bal. 8,000 Mark Thrasher, Drawing 312 Bal. 800 Income Summary 313 Lawn Service Fees 401 Bal. 5,000 Wages Expense 511 Bal. 400 Advertising Expense 512 Bal. 600 Travel Expense 515 Bal. 100 Supplies Expense 524 Bal. 900 Insurance Expense 535 Bal.…arrow_forwardTwo types of closing journal entries are posted to retained earnings at year-end. These are entries to: Multiple Choice transfer revenues and expenses to retained earnings. transfer assets and liabilities to retained earnings. transfer net income (or loss) and dividends declared to retained earnings. close permanent and temporary accounts. 50 TBUR Nextarrow_forward

- CLOSING ENTRIES Using the spreadsheet and partially completed Income Summary Account on page 605 prepare the following:1. Closing entries for Balloons and Baubbles in a general journal.2. A post-closing trial balance.arrow_forwardJournalize the closing entries necessary to close out all the temporary accounts.arrow_forwardReconstruction of Closing Entries The following T accounts summarize entries made to selected general ledger accounts of Cooper $ Company. Certain entries, dated December 31, are closing entries. Prepare the closing entries that were made on December 31.arrow_forward

- After the adjusting entries are recorded and posted and the financial statements have been prepared, you are ready to record the closing entries. Closing entries zero out the temporary owners equity accounts (revenue(s), expenses(s), and Drawing). This process transfers the net income or net loss and the withdrawals to the Capital account. In addition, the closing process prepares the records for the new fiscal period. Required 1. Journalize the dosing entries in the general journal. (If you are using Working Papers to prepare the closing entries, enter your transactions beginning on page 5.) 2. Post the closing entries to the general ledger accounts. (Skip this step if you are using CLGL.) 3. Prepare a post-dosing trial balance as of October 31, 20--. Check Figures 1. Debit to Income Summary second entry, 12,023.25 2. Post-closing trial balance total, 37,420.00arrow_forwardClosing Entries Lloyd Bookstore shows the following dividends, revenue, and expense account balances before closing: Required: Prepare closing entries.arrow_forwardUse the following information to answer Exercises E5-23 through E5-25. The adjusted trial balance of Quality Office Systems at March 31, 2018, follows: Journalizing closing entries Requirements Journalize the required dosing entries at March 31, 2018. Set up T-accounts for Income Summary; Retained Earnings; and Dividends. Post the closing entries to the T-accounts, and calculate their ending balances. How much was Quality Office’s net income or net loss?arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning