Videos

Refer to the data in Exercise 6-39. The president of Tiger Furnishings is confused about the differences in costs that result from using direct labor costs and machine-hours.

Required

- a. Explain why the two product costs are different.

- b. How would you respond to the president when asked to recommend one allocation base or the other?

- c. The president says to choose the allocation base that results in the highest income. Is this an appropriate basis for choosing an allocation base?

a.

Explain the difference between the two products costs.

Explanation of Solution

Product cost:

Product cost includes all the costs that are attributed to the production of the product. All the money that has spent on the process of production or purchase of the product is known as product cost.

Product cost per unit:

The product cost per unit is determined by dividing the total of variable and fixed cost with the total number of units.

Predetermined overhead rate:

The predetermined overhead rate is the rate computed for applying manufacturing overheads to the work-in-process inventory. This rate can be computed by dividing the total amount of manufacturing overheads by the base of allocation.

Difference between the two products costs:

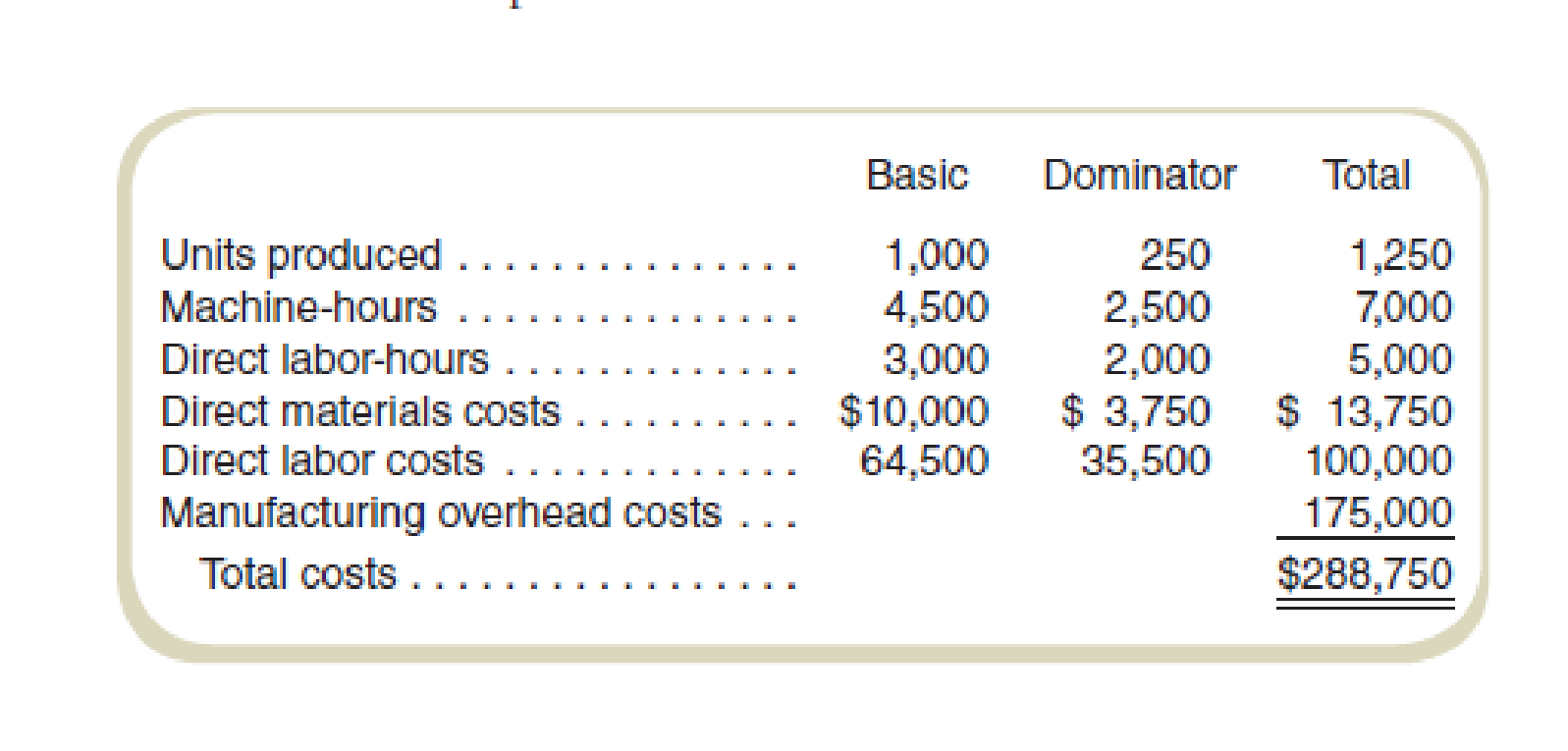

While using direct-labor costs the allocation of overheads is as follows:

For Product B: $112,875 (2)

For Product D: $62,125 (3)

And,

While using Machine-hours the allocation of overheads is as follows:

For Product B: $112,500 (5)

For Product D: $62,500 (6)

This shows the difference between the two methods of allocation is either increase or decrease of $375. This difference exists due to the different bases used for the calculation of predetermined rates. If the direct-labor costs are used then the resulting predetermined rate is $1.75 or 175% approximately. The process is oriented in terms of the base of direct-labor costs.

But, when machine-hours are used for the allocation of overheads with respect to the predetermined rate the resulting $25 will be giving a different result. The base for Compute both the predetermined rates is different.

The sum of allocation would be $175,000 for either method used for Compute cost allocation. But the allocations to both the products using the different methods would be different. The reason for this is that when direct-labor costs are used as a base the result is computed using direct-labor costs. But, when machine-hours are used as a base the computed result would be with respect to the machine-hours.

Thus, the allocation of overheads differs due to a different base of allocation used.

Working note 1:

Compute the predetermined overhead rate using direct labor costs as the base for allocation:

Working note 2:

Allocation of predetermined overhead costs using direct labor costs as the base for allocation:

For Basic:

For Dominator:

Working note 3:

The predetermined overhead rate while using machine-hours for cost allocation:

Working note 4:

Allocation of predetermined overhead costs using machine-hours as the base for allocation:

For Basic:

For Dominator:

b.

Describe the points to be taken into consideration when recommending one allocation base or the other.

Explanation of Solution

The points to be taken into consideration when recommending one allocation base or the other:

1) The method of production that is being used by the company in accordance with the operations and the availability of the resources.

2) The pooling of cost should be done but should correspond to the process of allocation that represents an accurate picture.

3) Either of the cost systems can be used as they both represent an accurate picture. But, if the product is labor intensive then the use of labor-hours cost is recommended. It would present facts clearly.

Hence, the recommendations to use any base for allocation should be in accordance with the production process. The company can use two-stage allocation for allocation of overheads.

c.

Comment on whether using the allocation base that results in the highest income is appropriate or not.

Explanation of Solution

It is not appropriate to choose the highest income generating base for the allocation of cost. The consideration should be to report the data accurately and consistently. While choosing the base to allocate the cost, the cost system should be in accordance with the base that is being used by the process and not the base which is generating more income.

Hence, the base that results in highest income should not be used as this is not an appropriate basis for choosing an allocation base.

Want to see more full solutions like this?

Chapter 6 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Discuss how, as warehouse manager for Vinnies Vinyls, you view the different rate of allocated costs the warehouse is being charged compared to the West store. Describe the implications of this. What steps could you take to solve this discrepancy? What alternatives would you consider, assuming management is willing to consider making changes in the rate?arrow_forwardAs manager of department B in MarIeys Manufacturing, based on the costs you identified in the previous exercise for further research, how does this impact the financial performance of your department, and what might be some questions you want to ask or solutions you might propose to Marleys management?arrow_forwardWhich of the following statements regarding activity-based costing (ABC) is false? A. ABC is not an appropriate tool for analysing non-manufacturing costs. B. ABC can be used to analyse the profitability of customers. C. ABC evolved as a response to problems with traditional costing systems. D. ABC can be used to measure the cost of cost objects.arrow_forward

- It is known that a new fee will increase if the order made by the customer increases. Based on this information, the cost is included in the cost hierarchy category? a. customer -batch level cost b.customer output unit-level costs c.customer cost d. division sustaining costs e. there is no right answerarrow_forwardWhich of the following statements is incorrect? O A. If MOH is overallocated to a job that has been sold, and the company calculates sales price by marking up job costs, the job will likely be underpriced. O B. The formula to arrive at the POHR is total budgeted manufacturing overhead divided by total estimated allocation base. O C. To calculate the increase to WIP for allocated MOH costs, the POHR is multiplied by the actual amount of the allocation based used by the cost object. D. "Number of units" is typically not an appropriate allocation base for MOH because the company's products do not consume equal overhead resources. If the over/underallocated MOH is fairly large and the majority of the units have not been sold, the balance in MOH should be prorated between WIP, FG, and COGS. O E.arrow_forwardWhich one of the following is an example of a committed cost? O a. The salary of the marketing manager O b. None of the given answers С. The cost of employee training program O d. The salary of the chief operating officer e. The cost of annual end of year celebrationarrow_forward

- a. Mr. Smith, the financial controller of LabAid, is convinced that the step-down method allocates more costs to the operating departments than does the direct method. Do you agree with Mr. Smith? Explain. b. Assume that you are the manager of the Daily Patient department. Discuss which method of cost allocation would you prefer. Justify your decision.arrow_forwardWhich of the following statements is not a characteristic of a target costing system? It is a good system to compare the cost of your products with that of your competitors Assists with ensuring that a business can achieve its desired profit levels Focuses on cost reductions after the product has been designed Focuses on the manufacturing processes to see if improvements can be made from a cost perspective.arrow_forwardDifferential costs represent – Group of answer choices the costs which is shown in the balance sheet but not expensed in the income statement until the sale of the products. The differences in costs among different departments of an organization. the amount of increase or decrease in costs from a particular course of action when compared to its alternatives the difference between controllable costs and non-controllable costs.arrow_forward

- 4) Design ABC system for EON and Brothers (discuss steps) 5) What are the Costs per unit of Alfa and Beta under traditional and ABC costing systems?What would be the prices of Alpha and Beta traditional and ABC costing systems? Comparethe costs and prices calculated in the two systems (Calculations should be shown in theappendix) and for analysis 6) Discuss your recommendation on the viability of ABC for EON and Brothers Ltd., given thefinancial director's concerns.arrow_forwardWhich of the following statements is false? Multiple Choice Examples of selling costs include shipping, sales commissions, and costs of finished goods warehouses. Discretionary fixed costs may be altered in the short term by current managerial decisions. A particular cost may be direct or indirect depending on the cost object. All sunk costs should be ignored in making a decision. Some of the conversion costs are period costs.arrow_forwardWhich one of the following is an example of a committed cost? a. The salary of the marketing manager O b. The salary of the chief operating officer O c. None of the given answers O d. The cost of employee training program O e. The cost of annual end of year celebrationarrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub