Concept explainers

Videos

Complete accounting cycle

For the past several years, Jeff Horton has operated a part-time consulting business from his home. As of April 1, 2018, Jeff decided to move to rented quarters and to operate the business, which was to be known as Rosebud Consulting, on a full-time basis. Rosebud entered into the following transactions during April:

| Apr. 1. | The following assets were received from Jeff Horton in exchange for common stock: cash, $20,000; accounts receivable, $14,700; supplies, $3,300; and office equipment, $12,000. There were no liabilities received. |

| 1. | Paid three months' rent on a lease rental contract, $6,000. |

| 2. | Paid the premiums on property and casualty insurance policies, $4,200. |

| 4. | Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, $9,400. |

| 5. | Purchased additional office equipment on account from Smith Office Supply Co., $8,000. |

| 6. | Received cash from clients on account, $11,700. |

| 10. | Paid cash for a newspaper advertisement, $350. |

| 12. | Paid Smith Office Supply Co. for part of the debt incurred on April 5, $6,400. |

| 12. | Recorded services provided on account for the period April1-12, $21,900. |

| 14. | Paid receptionist for two weeks’ salary, $1,650. |

| Record the following transactions on Page 2 of the journal: | |

| 17. | Recorded cash from cash clients for fees earned during the period Apri11-16, $6,600. |

| 18. | Paid cash for supplies, $725. |

| 20. | Recorded services provided on account for the period April13-20, $16,800. |

| 24. | Recorded cash from cash clients for fees earned for the period April 17-24, $4,450. |

| 26. | Received cash from clients on account, $26,500. |

| 27. | Paid receptionist for two weeks’ salary, $1,650. |

| 29. | Paid telephone bill for April, $540. |

| 30. | Paid electricity bill for April, $760. |

| 30. | Recorded cash from cash clients for fees earned for the period April 25-30, $5,160. |

| 30. | Recorded services provided on account for the remainder of April, $2,590. |

| 30. | Paid dividends, $18,000. |

Instructions

- 1. Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.)

11 Cash

12 Accounts Receivable

14 Supplies

15 Prepaid Rent

16 Prepaid Insurance

18 Office Equipment

19 Accumulated Depreciation

21 Accounts Payable

22 Salaries Payable

23 Unearned Fees

31 Common Stock

32

Retained Earnings 33 Dividends

41 Fees Earned

51 Salary Expense

52 Supplies Expense

53 Rent Expense

54 Depreciation Expense

55 Insurance Expense

59 Miscellaneous Expense

- 2. Post the journal to a ledger of four-column accounts.

- 3. Prepare an unadjusted

trial balance . - 4. At the end of April, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

- (A) Insurance expired during April is $350.

- (B) Supplies on hand on April 30 are $1,225.

- (C) Depreciation of office equipment for April is $400.

- (D) Accrued receptionist salary on April 30 is $275.

- (E) Rent expired during April is $2,000.

- (F) Unearned fees on April 30 are $2,350.

- 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet.

- 6. Journalize and post the

adjusting entries . Record the adjusting entries on Page 3 of the journal. - 7. Prepare an adjusted trial balance.

- 8. Prepare an income statement, a retained earnings statement, and a

balance sheet . - 9. Prepare and

post the closing entries. Record the closing entries on Page 4 of the journal. (Income Summary is account #34 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. - 10. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To journalize: The transactions of April in a two column journal beginning on page 1.

Explanation of Solution

Journalize the transactions of April in a two column journal beginning on page 1.

| Journal Page 1 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2018 | Cash | 11 | 20,000 | ||

| April | 1 | Accounts receivable | 12 | 14,700 | |

| Supplies | 14 | 3,300 | |||

| Office equipment | 18 | 12,000 | |||

| Common stock | 31 | 50,000 | |||

| (To record the receipt of assets) | |||||

| 1 | Prepaid Rent | 15 | 6,000 | ||

| Cash | 11 | 6,000 | |||

| (To record the payment of rent) | |||||

| 2 | Prepaid insurance | 16 | 4,200 | ||

| Cash | 11 | 4,200 | |||

| (To record the payment of insurance premium) | |||||

| 4 | Cash | 11 | 9,400 | ||

| Unearned fees | 23 | 9,400 | |||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Office equipment | 18 | 8,000 | ||

| Accounts payable | 21 | 8,000 | |||

| (To record the purchase of supplies of account) | |||||

| 6 | Cash | 11 | 11,700 | ||

| Accounts receivable | 12 | 11,700 | |||

| (To record the cash received from clients) | |||||

| 10 | Miscellaneousexpense | 59 | 350 | ||

| Cash | 11 | 350 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 12 | Accounts payable | 21 | 6,400 | ||

| Cash | 11 | 6,400 | |||

| (To record the payment made to creditors on account) | |||||

| 12 | Accounts receivable | 12 | 21,900 | ||

| Fees earned | 41 | 21,900 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 1,650 | ||

| Cash | 11 | 1,650 | |||

| (To record the payment made for salary) | |||||

Table (1)

| Journal Page 2 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2018 | Cash | 11 | 6,600 | ||

| April | 17 | Fees earned | 41 | 6,600 | |

| (To record the receipt of cash) | |||||

| 18 | Supplies | 14 | 725 | ||

| Cash | 11 | 725 | |||

| (To record the payment made for automobile expense) | |||||

| 20 | Accounts receivable | 12 | 16,800 | ||

| Fees earned | 41 | 16,800 | |||

| (To record the payment of advertising expense) | |||||

| 24 | Cash | 11 | 4,450 | ||

| Fees earned | 41 | 4,450 | |||

| (To record the cash received from client for fees earned) | |||||

| 26 | Cash | 11 | 26,500 | ||

| Accounts receivable | 12 | 26,500 | |||

| (To record the cash received from clients) | |||||

| 27 | Salary expense | 51 | 1,650 | ||

| Cash | 11 | 1,650 | |||

| (To record the payment of salary) | |||||

| 29 | Miscellaneous Expense | 59 | 540 | ||

| Cash | 11 | 540 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 760 | ||

| Cash | 11 | 760 | |||

| (To record the payment of electricity charges) | |||||

| 30 | Cash | 11 | 5,160 | ||

| Fees earned | 41 | 5,160 | |||

| (To record the cash received from client for fees earned) | |||||

| 30 | Accounts receivable | 12 | 2,590 | ||

| Fees earned | 41 | 2,590 | |||

| (To record the revenue earned and billed) | |||||

| 30 | Dividends | 33 | 18,000 | ||

| Cash | 11 | 18,000 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

To record: The balance of each accounts in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 20,000 | 20,000 | |||

| 1 | 1 | 6,000 | 14,000 | ||||

| 2 | 1 | 4,200 | 9,800 | ||||

| 4 | 1 | 9,400 | 19,200 | ||||

| 6 | 1 | 11,700 | 30,900 | ||||

| 10 | 1 | 350 | 30,500 | ||||

| 12 | 1 | 6,400 | 24,150 | ||||

| 14 | 1 | 1,650 | 22,500 | ||||

| 17 | 2 | 6,600 | 29,100 | ||||

| 18 | 2 | 725 | 28,375 | ||||

| 24 | 2 | 4,450 | 32,825 | ||||

| 26 | 2 | 26,500 | 59,325 | ||||

| 27 | 2 | 1,650 | 57,675 | ||||

| 29 | 2 | 540 | 57,135 | ||||

| 30 | 2 | 760 | 56,375 | ||||

| 30 | 2 | 5,160 | 61,535 | ||||

| 30 | 2 | 18,000 | 43,535 | ||||

Table (3)

| Account: Accounts ReceivableAccount no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 14,700 | 14,700 | |||

| 6 | 1 | 11,700 | 3,000 | ||||

| 12 | 1 | 21,900 | 24,900 | ||||

| 20 | 2 | 16,800 | 41,700 | ||||

| 26 | 2 | 26,500 | 15,200 | ||||

| 30 | 2 | 2,590 | 17,790 | ||||

Table (4)

| Account: SuppliesAccount no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 3,300 | 3,300 | |||

| 18 | 2 | 725 | 4,025 | ||||

| 30 | Adjusting | 3 | 2,800 | 1,225 | |||

Table (5)

| Account: Prepaid RentAccount no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 6,000 | 6,000 | |||

| 30 | Adjusting | 3 | 2,000 | 4,000 | |||

Table (6)

| Account: Prepaid InsuranceAccount no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 2 | 1 | 4,200 | 4,200 | |||

| 30 | Adjusting | 3 | 350 | 3,850 | |||

Table (7)

| Account: Office equipmentAccount no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 12,000 | 12,000 | |||

| 5 | 1 | 8,000 | 20,000 | ||||

Table (8)

| Account: Accumulated Depreciation-Office equipmentAccount no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 31 | Adjusting | 3 | 400 | 400 | ||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 5 | 1 | 8,000 | 8,000 | |||

| 12 | 1 | 6,400 | 1,600 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | Adjusting | 3 | 275 | 275 | ||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 4 | 1 | 9,400 | 9,400 | |||

| 30 | Adjusting | 3 | 7,050 | 2,350 | |||

Table (12)

| Account: Common StockAccount no.31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 1 | 50,000 | 50,000 | |||

Table (13)

| Account: Retained EarningsAccount no.32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 1 | 0 | |||||

| 30 | Closing | 4 | 53,775 | 53,775 | |||

| 30 | Closing | 4 | 18,000 | 35,775 | |||

Table (14)

| Account: Dividends Account no.33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | 2 | 18,000 | 18,000 | |||

| Closing | 4 | 18,000 | |||||

Table (15)

| Account: Income Summary Account no.34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | Closing | 4 | 64,550 | 64,550 | ||

| 30 | Closing | 4 | 10,775 | 53,775 | |||

| 30 | Closing | 4 | 53,775 | ||||

Table (16)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 12 | 1 | 21,900 | 21,900 | |||

| 17 | 2 | 6,600 | 28,500 | ||||

| 20 | 2 | 16,800 | 45,300 | ||||

| 24 | 2 | 4,450 | 49,750 | ||||

| 30 | 2 | 5,160 | 54,910 | ||||

| 30 | 2 | 2,590 | 57,500 | ||||

| 30 | Adjusting | 3 | 7,050 | 64,550 | |||

| 30 | Closing | 4 | 64,550 | ||||

Table (17)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 14 | 1 | 1,650 | 1,650 | |||

| 27 | 2 | 1,650 | 3,300 | ||||

| 30 | Adjusting | 3 | 275 | 3,575 | |||

| 30 | Closing | 4 | 3,575 | ||||

Table (18)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | Adjusting | 3 | 2,000 | 2,000 | ||

| 30 | Closing | 4 | 2,000 | ||||

Table (19)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | Adjusting | 3 | 2,800 | 2,800 | ||

| 30 | Closing | 4 | 2,800 | ||||

Table (20)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 30 | Adjusting | 3 | 400 | 400 | ||

| 30 | Closing | 4 | 400 | ||||

Table (21)

| Account: Insurance expense Account no.54 | ||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 2018 | ||||||||

| April | 30 | Adjusting | 3 | 350 | 350 | |||

| 30 | Closing | 4 | 350 | |||||

Table (22)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| April | 10 | 1 | 350 | 350 | |||

| 29 | 2 | 540 | 890 | ||||

| 31 | 2 | 760 | 1,650 | ||||

| 31 | Closing | 4 | 1,650 | ||||

Table (23)

(3)

To prepare: The unadjusted trial balance of Consulting R atApril, 30.

Explanation of Solution

Prepare an unadjusted trial balance of Consulting R for the month ended April, 30 as follows:

|

R Consulting Unadjusted Trial Balance April 30, 2018 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 43,535 | |

| Accounts receivable | 12 | 17,790 | |

| Supplies | 14 | 4,025 | |

| Prepaid rent | 15 | 6,000 | |

| Prepaid insurance | 16 | 4,200 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated depreciation-Office equipment | 19 | 0 | |

| Accounts payable | 21 | 1,600 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 9,400 | |

| Common stock | 31 | 50,000 | |

| Retained earnings | 32 | 0 | |

| Dividends | 33 | 18,000 | |

| Fees earned | 41 | 57,500 | |

| Salary expense | 51 | 3,300 | |

| Rent expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 0 | |

| Total | 118,500 | 118,500 | |

Table (22)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $118,800.

(5)

To enter: The unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

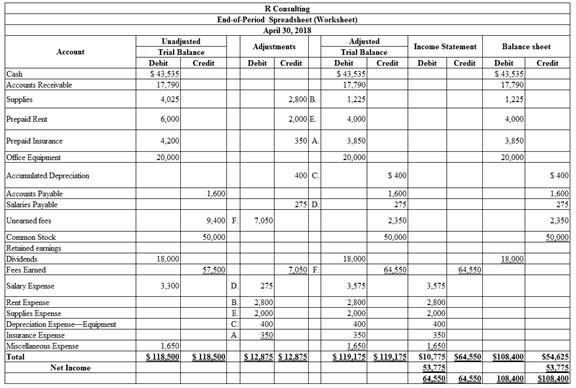

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (23)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(6)

To Journalize: Theadjusting entries of Consulting G for April 30.

Explanation of Solution

The adjusting entries of ConsultingG for April 30, 2018are as follows:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) |

|

| 2018 | Insurance expense | 55 | 350 | ||

| April | 30 | Prepaid insurance | 16 | 350 | |

| (To record the insurance expense for April) | |||||

| 30 | Supplies expense(1) | 52 | 2,800 | ||

| Supplies | 14 | 2,800 | |||

| (To record the supplies expense) | |||||

| 30 | Depreciation expense | 54 | 400 | ||

| Accumulated Depreciation | 19 | 400 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 30 | Salaries expense | 51 | 275 | ||

| Salaries payable | 22 | 275 | |||

| (To record the accrued salaries payable) | |||||

| 30 | Rent expense | 53 | 2,000 | ||

| Prepaid rent | 15 | 2,000 | |||

| (To record the rent expense for April) | |||||

| 30 | Unearned fees(2) | 23 | 7,050 | ||

| Fees earned | 41 | 7,050 | |||

| (To record the receipt of unearned fees) | |||||

Table (24)

Working notes:

(7)

To prepare: An adjusted trial balance of Consulting G for April 30, 2018.

Explanation of Solution

An adjusted trial balance of Consulting G for April 30, 2018 is prepared as follows:

|

G Consulting Adjusted Trial Balance April 30, 2018 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 43,535 | |

| Accounts receivable | 12 | 17,790 | |

| Supplies | 14 | 1,225 | |

| Prepaid rent | 15 | 4,000 | |

| Prepaid insurance | 16 | 3,850 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated Depreciation | 19 | 400 | |

| Accounts payable | 21 | 1,600 | |

| Salaries payable | 22 | 275 | |

| Unearned fees | 23 | 2,350 | |

| Common stock | 31 | 50,000 | |

| Retained earnings | 32 | 0 | |

| Dividends | 33 | 18,000 | |

| Fees earned | 41 | 64,550 | |

| Salary expense | 51 | 3,575 | |

| Supplies expense | 52 | 2,800 | |

| Rent Expense | 53 | 2,000 | |

| Depreciation expense | 54 | 400 | |

| Insurance expense | 55 | 350 | |

| Miscellaneous expense | 59 | 1,650 | |

| Total | 119,175 | 119,175 | |

Table (25)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $119,175.

(8)

To Prepare: An income statement for the year ended April 30, 2018.

Explanation of Solution

An income statement for the year ended April 30, 2018 is as follows:

| R Consulting | ||

| Income Statement | ||

| For the year ended April 30, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 64,550 | |

| Expenses: | ||

| Salaries Expense | 3,575 | |

| Rent Expense | 2,800 | |

| Supplies Expense | 2,000 | |

| Depreciation Expense- Building | 400 | |

| Insurance Expense | 350 | |

| Miscellaneous Expense | 1,650 | |

| Total Expenses | 10,775 | |

| Net Income | $53,775 | |

Table (26)

Hence, the net income of R Consultingfor the year ended April 30, 2018is $50,335.

To Prepare: The Earnings statement for the year ended April 30, 2018.

Explanation of Solution

The earnings statement for the year ended April 30, 2018 is as follows:

| R Consulting | ||

| Earnings Statement | ||

| For the Year Ended April 30, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Retained earnings, April 1, 2018 | 0 | |

| Add: Net income | 53,775 | |

| Less: Dividends | (18,000) | |

| Change in retained earnings | 35,775 | |

| Retained earnings, April 30, 2018 | $35,775 | |

Table (27)

Hence, retained earnings for the year ended April 30, 2018is $35,775.

To Prepare: The balance sheet of R Consultingat April 30, 2018.

Explanation of Solution

| R Consulting | |||

| Balance Sheet | |||

| April 30, 2018 | |||

| Assets | |||

| Current Assets: | $ | $ | |

| Cash | 43,535 | ||

| Accounts Receivable | 17,790 | ||

| Supplies | 1,225 | ||

| Prepaid Rent | 4,000 | ||

| Prepaid Insurance | 3,850 | ||

| Total Current Assets | 70,400 | ||

| Property, plant and equipment: | |||

| Office Equipment | 20,000 | ||

| Less: Accumulated Depreciation | 400 | ||

| Total Plant Assets | 19,600 | ||

| Total Assets | $90,000 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | 1,600 | ||

| Salaries Payable | 275 | ||

| Unearned rent | 2,350 | ||

| Total Liabilities | 4,225 | ||

| Stockholder’s Equity | |||

| Common stock | 50,000 | ||

| Retained earnings | 35,775 | ||

| Total stockholder’s equity | 85,775 | ||

| Total Liabilities and Stockholder’s Equity | $90,000 | ||

Table (28)

It is one of the financial statements, which shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the company has enough assets to pay off its liabilities.

Therefore, the total assets and total liabilities plus owners’ equity of Consulting RatApril 30, 2018is $90,000.

(9)

To Journalize: The closing entries for RConsulting.

Explanation of Solution

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| August 30, 2018 | Fees earned | 41 | 64,550 | |

| Income summary | 34 | 64,550 | ||

| (To close the balances of revenue account) | ||||

| August 30, 2018 | Income summary | 34 | 10,775 | |

| Salary expense | 51 | 3,575 | ||

| Supplies Expense | 52 | 2,800 | ||

| Rent Expense | 53 | 2,000 | ||

| Depreciation Expense | 54 | 400 | ||

| Insurance Expense | 55 | 350 | ||

| Miscellaneous Expense | 59 | 1,650 | ||

| (To close the balances of expense account) | ||||

| August 30, 2018 | Income summary | 34 | 53,775 | |

| Retained earnings | 32 | 53,775 | ||

| (To Close the excess of revenue to expenses) | ||||

| August 30, 2018 | Retained earnings | 32 | 18,000 | |

| Dividends | 33 | 18,000 | ||

| (To close the dividend account to retained earnings account) | ||||

Closing entry for revenue and expense accounts:

Table (4)

- Fees earned are revenue account. Since the amount of revenue is closed and transferred to Income summary account. Here, FI Services earned an income of $64,550. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expense, supplies Expense, Depreciation Expense, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Closing entries are also passed in order to close the excess of revenue over the expenses, and the dividend account.

(10)

To Journalize: The closing entries for RConsulting.

Explanation of Solution

Prepare apost–closing trial balance of RConsulting for the month ended April 30, 2018 as follows:

|

Company B Post-closing Trial Balance April, 30, 2018 |

|||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 43,535 | |

| Accounts receivable | 12 | 17,790 | |

| Supplies | 14 | 1,225 | |

| Prepaid rent | 15 | 4,000 | |

| Prepaid insurance | 16 | 3,850 | |

| Office Equipment | 18 | 20,000 | |

| Accumulated depreciation –Office Equipment | 19 | 400 | |

| Accounts payable | 21 | 1,600 | |

| Salaries payable | 22 | 275 | |

| Unearned rent | 23 | 2,350 | |

| Common stock | 31 | 50,000 | |

| Retained earnings | 32 | 35,775 | |

| Total | 90,400 | 90,400 | |

Table (5)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $90,400

Want to see more full solutions like this?

Chapter 4 Solutions

Corporate Financial Accounting

- Scenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. Paid three (3) months rent on a lease rental contract, $6,000. Paid the premiums on the property and peril insurance policies, $3,000. Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. Purchased additional office equipment on…arrow_forwardScenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. 2.Paid three (3) months rent on a lease rental contract, $6,000. 3.Paid the premiums on the property and peril insurance policies, $3,000. 4.Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. 5.Purchased additional office equipment on account from…arrow_forwardScenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. 2. Paid three (3) months rent on a lease rental contract, $6,000. 3. Paid the premiums on the property and peril insurance policies, $3,000. 4. Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. 5. Purchased additional office equipment on account from…arrow_forward

- Scenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. Paid three (3) months rent on a lease rental contract, $6,000. Paid the premiums on the property and peril insurance policies, $3,000. Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. Purchased additional office equipment on…arrow_forwardScenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. Paid three (3) months rent on a lease rental contract, $6,000. Paid the premiums on the property and peril insurance policies, $3,000. Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. Purchased additional office equipment on…arrow_forwardScenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. 2.Paid three (3) months rent on a lease rental contract, $6,000. 3.Paid the premiums on the property and peril insurance policies, $3,000. 4.Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. 5.Purchased additional office equipment on account from…arrow_forward

- T Account entries for Simple Construction:Bob Simple graduated from the BCIT Construction Management Program and decided to start his own construction company. We will record various entries that might be made in a T account sheet in order to account for his second year of operations. At the end of the first year, his income statement and balance sheet havethe following values:Balance Sheet Entries for Last Year:Cash: 365,000Accounts Receivable: $17,000Materials Inventory: $2000Equipment: $15,000Accumulated Amortization: $500Accounts Payable: $22,000Bank Loan –Long Term: $10,000Dividend Payable: $35,000Interest Payable: $500Wages Payable: $5,000Common Stock: $250,000Retained Earnings: $76,000Income statement Final Entries for Last Year:Revenue: $145,000Materials Expense: $20,000Wages Expense: $10,000Amortization Expense: $500Rental Expense: $2,500Interest Expense: $1000Net Income: $111,000 Question 1a.Enter the relevant amounts in the T sheet to start the current year, and designate…arrow_forwardScenario: Ralph Collins founded Collins Consignment Sales Company and the company was operated from his home. As of September 1, 2021, Collins decided to move to rented quarters and to operate the business on a full-time basis. He wishes to know how much net income the business has earned but has no prior knowledge of accounting and has approached your group for advice. The company entered the following transactions during September: Sept 1. The following assets were received from Ralph in exchange for capital of Collins Consignment Sales Company: cash - $19,000, accounts receivable - $2,800, supplies - $2,050, and office equipment - $15,000. There were no liabilities received. Paid three (3) months rent on a lease rental contract, $6,000. Paid the premiums on the property and peril insurance policies, $3,000. Received cash from clients as an advance payment for services to be provided in the coming months, $5,900. Purchased additional office equipment on…arrow_forwardProcedures: 1. Analyze the following business transactions below. For the month of December 2022, Mr. Mira Shikigami had the following transactions: Dec. Mr. Mira Shikigami invested P1,200,000 to start the business, Shikigami Accounting Firm 1 1 The firm obtained a note from Solar Bank amounting to P300,000. The note bears a 6% annual interest payable every June 1 of the following year. The principal is payable in two (2) equal annual installments. 1 The firm paid P15,000 for the necessary permits and licenses for its operation. 1 The firm paid P180,000 for the annual rent of the office space. The lease contract will expire on June 1 of the following year and will be renewed yearly. 3 The firm rendered service to Kyubi Realties, Inc. worth P250,000 on credit. 3 The firm purchased supplies worth P50,000. 9 The firm purchased a laptop in cash, P50,000. The laptop has an estimated useful life of three (3) years with no residual value. The company treats purchases during the first half of…arrow_forward

- The first project for the semester will involve the following items to turn in: 1) Journal entries for financial transactions I will provide you. 2) An adjusted trial balance. 3) An Income statement. 1) On December 1 of 2019 Harold Hammer deposited $ 15,100 in a bank account in the name of Huaning Corporation in exchange for shares of common stock in the corporation. 2) On December 1 of 2019 Huaning Corporation purchased supplies on account for $ 226 . 3) On December 4 of 2019 Huaning Corporation received cash of $ 384 for product sold to the customer. 4) On December 5 of 2019 Huaning Corporation paid the vendor for the December 1st purchase of supplies. 5) On December 6 of 2019 Huaning Corporation purchases supplies on account for $ 469 .6) On December 8 of 2019 Huaning Corporation sells product for $ 445 on account to a customer.7) On December 9 of 2019 Huaning Corporation sells product for $ 462 on account to a customer. 8) On December 10 of 2019 Huaning Corporation paid, in…arrow_forwardThe accounting records and bank statement of Orison Supply Store provide the following information at the end of April. The closing 'Cash' account balance was $28,560, and the bank statement shows a closing balance of $32,000. On reviewing the bank statement it is found an account customer has deposited $2,000 into the bank account for a March sale and the monthly insurance premium of $4,500 was automatically charged to the account. Interest of $5,10 was paid by the bank and a bank fee of $50 was charged to the account. A payment of $1,500 to a supplier has been recorded twice in the accounts. After the ,calculation of the "ending reconciled cash balance", what is the balance of the 'cash' account?arrow_forwardDean Winchester opened Ghost Cleaners on June 1, 2021. He is the sole owner of the corporation.During June, the following transactions were completed by Dean.1-Jun Invested $65,000 in exchange for common stock in Ghost Cleaners, Inc.1-Jun Purchased a used van for $12,000, paying $3,000 cash and the taking out a note payable for the rest.He plans to pay off the remaining balance on the van by June 1, 2022. The note has a 10% APRwith interest being payable at the end of every month. No principle payments are due until August 1, 2021.1-Jun Paid $1,800 cash on a 12-month insurance policy effective June 1, 2021.1-Jun Hired his brother, Sam, to help with the corporation. He will be paid $1,000 per month for now.5-Jun Purchased cleaning supplies for $1,500 on account.7-Jun Billed a client, F. Crowley, for services performed on June 7 in the amount of $3,000.8-Jun Paid $100 for gasoline for the van.12-Jun Paid $200 for maintenance on the van.15-Jun Incurred wages expense of $2,000.16-Jun…arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT