Videos

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234. Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after the addition of the new product. In the last two years, however, the plant faced intense competition, and its sales of Part #127 dropped. In fact, the plant showed a small loss in the most recent reporting period. Much of the competition was from foreign sources, and the plant manager was convinced that the foreign producers were guilty of selling the part below the cost of producing it. The following conversation between Patty Goodson, plant manager, and Joseph Fielding, divisional marketing manager, reflects the concerns of the division about the future of the plant and its products.

JOSEPH: You know, Patty, the divisional manager is real concerned about the plant’s trend. He indicated that in this budgetary environment, we can’t afford to carry plants that don’t show a profit. We shut one down just last month because it couldn’t handle the competition.

PATTY: Joe, you and I both know that Part #127 has a reputation for quality and value. It has been a mainstay for years. I don’t understand what’s happening.

JOSEPH: I just received a call from one of our major customers concerning Part #127. He said that a sales representative from another firm offered the part at $20 per unit—$11 less than what we charge. It’s hard to compete with a price like that. Perhaps the plant is simply obsolete.

PATTY: No. I don’t buy that. From my sources, I know we have good technology. We are efficient. And it’s costing a little more than $21 to produce that part. I don’t see how these companies can afford to sell it so cheaply. I’m not convinced that we should meet the price. Perhaps a better strategy is to emphasize producing and selling more of Part #234. Our margin is high on this product, and we have virtually no competition for it.

JOSEPH: You may be right. I think we can increase the price significantly and not lose business. I called a few customers to see how they would react to a 25 percent increase in price, and they all said that they would still purchase the same quantity as before.

PATTY: It sounds promising. However, before we make a major commitment to Part #234, I think we had better explore other possible explanations. I want to know how our production costs compare to those of our competitors. Perhaps we could be more efficient and find a way to earn our normal return on Part #127. The market is so much bigger for this part. I’m not sure we can survive with only Part #234. Besides, my production people hate that part. It’s very difficult to produce.

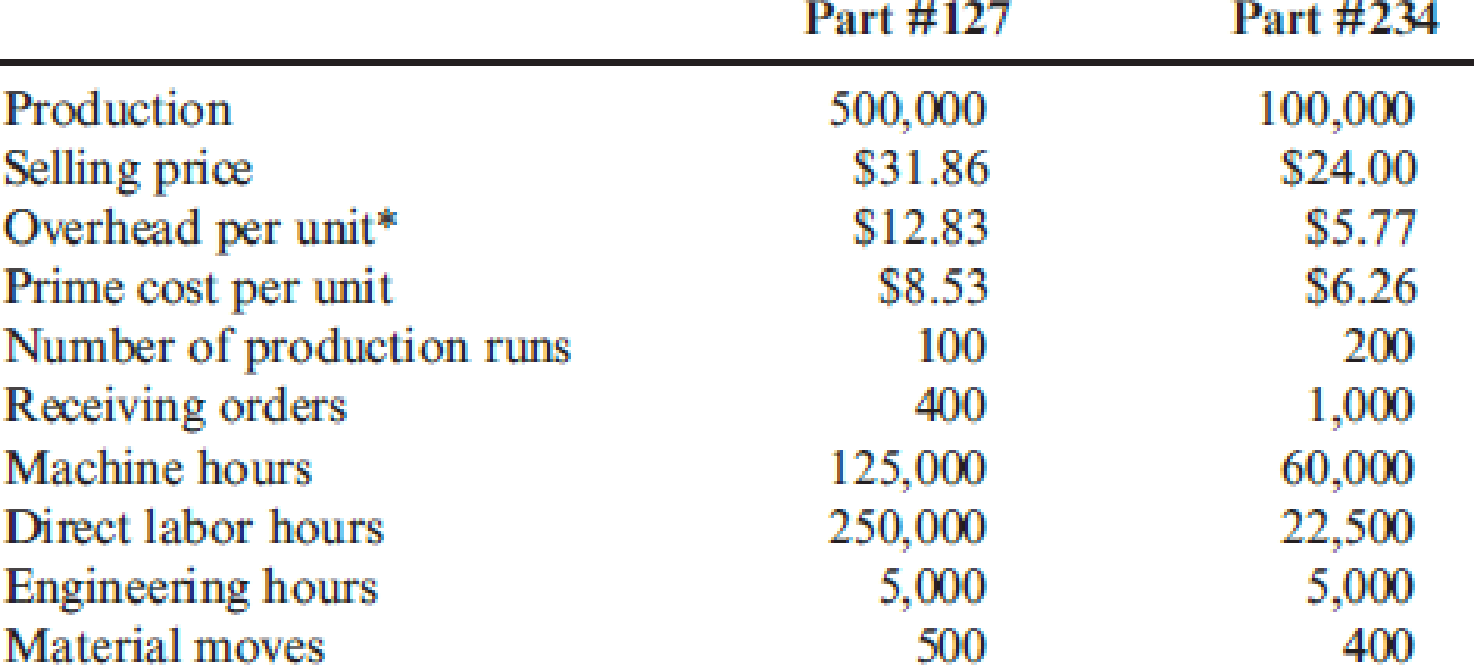

After her meeting with Joseph, Patty requested an investigation of the production costs and comparative efficiency. She received approval to hire a consulting group to make an independent investigation. After a three-month assessment, the consulting group provided the following information on the plant’s production activities and costs associated with the two products:

* Calculated using a plantwide rate based on direct labor hours. This is the current way of assigning the plant’s

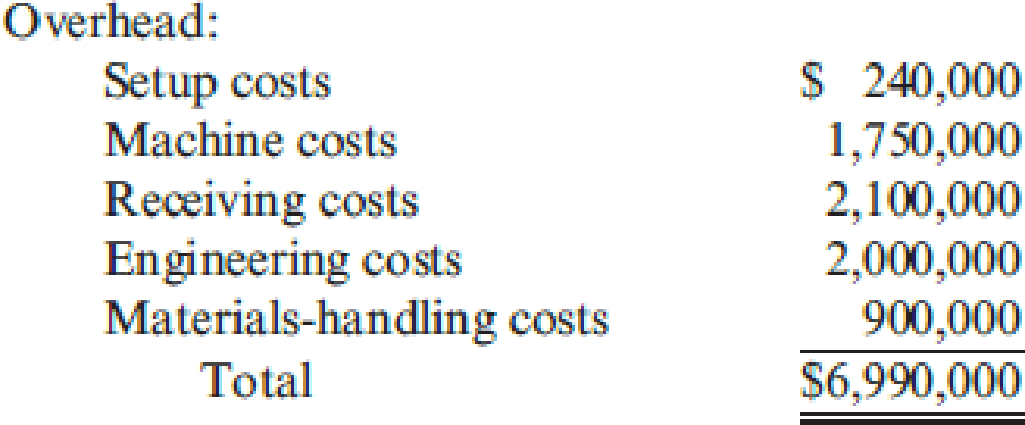

The consulting group recommended switching the overhead assignment to an activity-based approach. It maintained that activity-based cost assignment is more accurate and will provide better information for decision making. To facilitate this recommendation, it grouped the plant’s activities into homogeneous sets with the following costs:

Required:

- 1. Verify the overhead cost per unit reported by the consulting group using direct labor hours to assign overhead. Compute the per-unit gross margin for each product.

- 2. After learning of activity-based costing, Patty asked the controller to compute the product cost using this approach. Recompute the unit cost of each product using activity-based costing. Compute the per-unit gross margin for each product.

- 3. Should the company switch its emphasis from the high-volume product to the low-volume product? Comment on the validity of the plant manager’s concern that competitors are selling below the cost of making Part #127.

- 4. Explain the apparent lack of competition for Part #234. Comment also on the willingness of customers to accept a 25 percent increase in price for Part #234.

- 5. Assume that you are the manager of the plant. Describe what actions you would take based on the information provided by the activity-based unit costs.

Trending nowThis is a popular solution!

Chapter 4 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Bienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct…arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct…arrow_forward

- Weston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular…arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular…arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular…arrow_forward

- Weston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct materials cost per unit $50.00 $30.00 Direct…arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct…arrow_forwardWeston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct…arrow_forward

- Weston Corporation manufactures a product that is available in both a deluxe and a regular model. The company has made the regular model for years; the deluxe model was introduced several years ago to tap a new segment of the market. Since introduction of the deluxe model, the company’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly. Overhead is applied to products on the basis of direct labor-hours. At the beginning of the current year, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regular model. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular model requires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct materials cost per unit $50.00 $30.00 Direct labor cost per unit $30.00…arrow_forwardAlberta Gauge Company, Ltd., a small manufacturing company in Calgary, Alberta, manufactures three types of electrical gauges used in a variety of machinery. For many years the company has been profitable and has operated at capacity. However, in the last two years, prices on all gauges were reduced and selling expenses increased to meet competition and keep the plant operating at capacity. Second-quarter results for the current year, which follow, typify recent experience. Alice Carlo, the company’s president, is concerned about the results of the pricing, selling, and production prices. After reviewing the second-quarter results, she asked her management staff to consider the following three suggestions: Discontinue the R-gauge line immediately. R-gauges would not be returned to the product line unless the problems with the gauge can be identified and resolved. Increase quarterly sales promotion by $100,000 on the Q-gauge product line in order to increase sales volume by 15 percent.…arrow_forwardBramble Pix currently uses a six-year-old molding machine to manufacture silver picture frames. The company paid $88,000 for the machine, which was state of the art at the time of purchase. Although the machine will likely last another ten years, it will need a $12,000 overhaul in four years. More important, it does not provide enough capacity to meet customer demand. The company currently produces and sells 11,000 frames per year, generating a total contribution margin of $85,500. Martson Molders currently sells a molding machine that will allow Bramble Pix to increase production and sales to 15,000 frames per year. The machine, which has a ten-year life, sells for $131,000 and would cost $12,000 per year to operate. Bramble Pix's current machine costs only $8,000 per year to operate. If Bramble Pix purchases the new machine, the old machine could be sold at its book value of $5,000. The new machine is expected to have a salvage value of $19,500 at the end of its ten-year life.…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning