Concept explainers

Videos

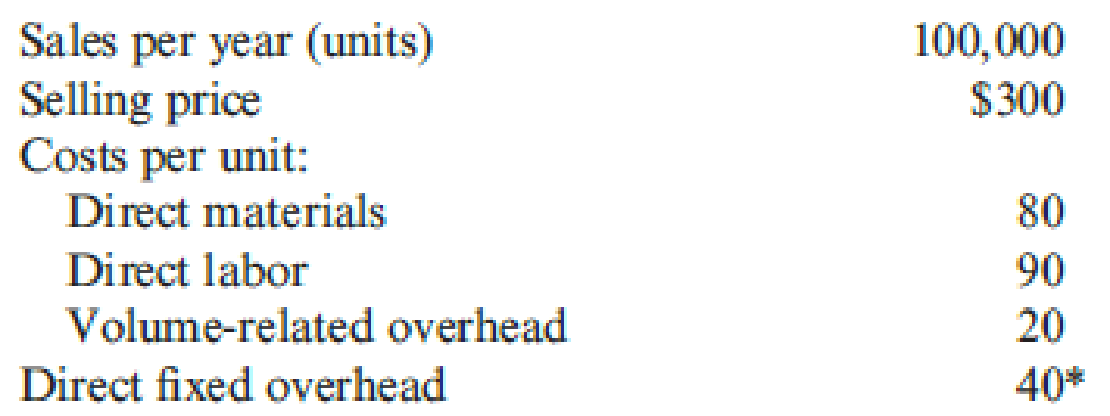

Mallette Manufacturing, Inc., produces washing machines, dryers, and dishwashers. Because of increasing competition, Mallette is considering investing in an automated manufacturing system. Since competition is most keen for dishwashers, the production process for this line has been selected for initial evaluation. The automated system for the dishwasher line would replace an existing system (purchased one year ago for $6 million). Although the existing system will be fully

The existing system is capable of producing 100,000 dishwashers per year. Sales and production data using the existing system are provided by the Accounting Department:

*All cash expenses with the exception of depreciation, which is $6 per unit. The existing equipment is being depreciated using straight-line with no salvage value considered.

The automated system will cost $34 million to purchase, plus an estimated $20 million in software and implementation. (Assume that all investment outlays occur at the beginning of the first year.) If the automated equipment is purchased, the old equipment can be sold for $3 million.

The automated system will require fewer parts for production and will produce with less waste. Because of this, the direct material cost per unit will be reduced by 25 percent. Automation will also require fewer support activities, and as a consequence, volume-related overhead will be reduced by $4 per unit and direct fixed overhead (other than depreciation) by $17 per unit. Direct labor is reduced by 60 percent. Assume, for simplicity, that the new investment will be depreciated on a pure straight-line basis for tax purposes with no salvage value. Ignore the half-life convention.

The firm’s cost of capital is 12 percent, but management chooses to use 20 percent as the required

Required:

- 1. Compute the

net present value for the old system and the automated system. Which system would the company choose? - 2. Repeat the net present value analysis of Requirement 1, using 12 percent as the discount rate.

- 3. Upon seeing the projected sales for the old system, the marketing manager commented: “Sales of 100,000 units per year cannot be maintained in the current competitive environment for more than one year unless we buy the automated system. The automated system will allow us to compete on the basis of quality and lead time. If we keep the old system, our sales will drop by 10,000 units per year.” Repeat the net present value analysis, using this new information and a 12 percent discount rate.

- 4. An industrial engineer for Mallette noticed that salvage value for the automated equipment had not been included in the analysis. He estimated that the equipment could be sold for $4 million at the end of 10 years. He also estimated that the equipment of the old system would have no salvage value at the end of 10 years. Repeat the net present value analysis using this information, the information in Requirement 3, and a 12 percent discount rate.

- 5. Given the outcomes of the previous four requirements, comment on the importance of providing accurate inputs for assessing investments in automated manufacturing systems.

1.

Ascertain the net present value for both the old and automated system, and state the system that the company would choose.

Explanation of Solution

Net present value method (NVP): Net present value method is the method which is used to compare the initial cash outflow of investment with the present value of its cash inflows. In the net present value, the interest rate is desired by the business based on the net income from the investment, and it is also called as the discounted cash flow method.

Ascertain the net present value for both the old and automated system, and state the system that the company would choose:

For Old system (in thousands):

| Year | Revenue | Expenses | Depreciation after tax | Cash flow | Discount factor @ 20% | Present value |

| (1) (a) | (2) (b) | (3) (c) | (e) | |||

| 1 | $18,000 | ($13,440) | $240 | 4,800 | 0.833 | 3,998 |

| 2 | $18,000 | ($13,440) | $240 | 4,800 | 0.694 | 3,331 |

| 3 | $18,000 | ($13,440) | $240 | 4,800 | 0.579 | 2,779 |

| 4 | $18,000 | ($13,440) | $240 | 4,800 | 0.482 | 2,314 |

| 5 | $18,000 | ($13,440) | $240 | 4,800 | 0.402 | 1,930 |

| 6 | $18,000 | ($13,440) | $240 | 4,800 | 0.335 | 1,608 |

| 7 | $18,000 | ($13,440) | $240 | 4,800 | 0.279 | 1,339 |

| 8 | $18,000 | ($13,440) | $240 | 4,800 | 0.233 | 1,118 |

| 9 | $18,000 | ($13,440) | $240 | 4,800 | 0.194 | 931 |

| 10 | $18,000 | ($13,440) | - | 4,560 | 0.162 | 739 |

| 20,088 | ||||||

| Less: Initial investment | 0 | |||||

| Net present value | 20,088 | |||||

Table (1)

Working note (1):

Compute the amount of revenue:

Working note (2):

Compute the amount of expense:

Working note (3):

Compute the amount of after tax depreciation expense:

For New system (in thousands):

| Year | Revenue | Expenses | Depreciation after tax | Cash flow | Discount factor | Present value |

| (1) (a) | (4) (b) | (6) (c) | (e) | |||

| 0 | (50,040) (7) | 1.000 | $(50,040) | |||

| 1 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.833 | 3,998 |

| 2 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.694 | 3,331 |

| 3 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.579 | 2,779 |

| 4 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.482 | 2,314 |

| 5 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.402 | 1,930 |

| 6 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.335 | 1,608 |

| 7 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.279 | 1,339 |

| 8 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.233 | 1,118 |

| 9 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.194 | 931 |

| 10 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.162 | 739 |

| Net present value | 2,025 | |||||

Table (2)

Working note (4):

Step 1: Compute the total cost:

| Particulars | Total cost |

| Direct materials | $60 |

| Direct labor | $36 |

| Volume-related overhead | $16 |

| Direct fixed overhead | $17 |

| Unit cost | $129 |

Table (3)

Step 2: Compute the amount of expense:

Working note (5):

Compute the loss on sale of old machinery:

Working note (6):

Compute the depreciation expense for cash outflow:

Working note (7):

Compute the cash outflow:

Description:

The company should choose the old system because it has the higher net present value.

2.

Ascertain the net present value for both the old and automated system under 12% discount rate, and state the system that the company would choose.

Explanation of Solution

Ascertain the net present value for both the old and automated system under 12% discount rate, and state the system that the company would choose:

For Old system (in thousands):

| Year | Revenue | Expenses | Depreciation after tax | Cash flow | Discount factor | Present value |

| (1) (a) | (2) (b) | (3) (c) | (e) | |||

| 1 | $18,000 | ($13,440) | $240 | 4,800 | 0.893 | 4,286 |

| 2 | $18,000 | ($13,440) | $240 | 4,800 | 0.797 | 3,826 |

| 3 | $18,000 | ($13,440) | $240 | 4,800 | 0.712 | 3,418 |

| 4 | $18,000 | ($13,440) | $240 | 4,800 | 0.636 | 3,053 |

| 5 | $18,000 | ($13,440) | $240 | 4,800 | 0.567 | 2,722 |

| 6 | $18,000 | ($13,440) | $240 | 4,800 | 0.507 | 2,434 |

| 7 | $18,000 | ($13,440) | $240 | 4,800 | 0.452 | 2,170 |

| 8 | $18,000 | ($13,440) | $240 | 4,800 | 0.404 | 1,939 |

| 9 | $18,000 | ($13,440) | $240 | 4,800 | 0.361 | 1,733 |

| 10 | $18,000 | ($13,440) | - | 4,560 | 0.322 | 1,468 |

| 27,048 | ||||||

| Less: Initial investment | 0 | |||||

| Net present value | 27,048 | |||||

Table (4)

For New system (in thousands):

| Year | Revenue | Expenses | Depreciation after tax | Cash flow | Discount factor | Present value |

| (1) (a) | (4) (b) | (6) (c) | (e) | |||

| 0 | (50,040) (7) | 1.000 | $(50,040) | |||

| 1 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.893 | 11,091 |

| 2 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.797 | 9,899 |

| 3 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.712 | 8,843 |

| 4 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.636 | 7,899 |

| 5 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.567 | 7,042 |

| 6 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.507 | 6,297 |

| 7 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.452 | 5,614 |

| 8 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.404 | 5,018 |

| 9 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.361 | 4,484 |

| 10 | $18,000 | ($7,740) | $2,160 | 12,420 | 0.322 | 3,999 |

| Net present value | 20,145 | |||||

Table (5)

Description:

The company should choose the old system because it has the higher net present value. However when using 12% discount rate, the automated system becomes more attractive because under 10% discount rate the NPV was $ 2,025, whereas under 12% discount rate the NPV was $ 20,145.

3.

Ascertain the net present value for the 12% discount rate using this given information.

Explanation of Solution

Ascertain the net present value for the 12% discount rate using this given information.

| Year | Revenue | Expenses | Depreciation after tax | Cash flow | Discount factor | Present value |

| (8) (a) | (9) (b) | (6) (c) | (e) | |||

| 0 | $0 | 1.000 | $0 | |||

| 1 | $18,000 | ($13,440) | $240 | 4,800 | 0.893 | 4,286 |

| 2 | $16,200 | (12,300) | $240 | 4,140 | 0.797 | 3,300 |

| 3 | $14,400 | (11,160) | $240 | 3,480 | 0.712 | 2,478 |

| 4 | $12,600 | (10,020) | $240 | 2,820 | 0.636 | 1,794 |

| 5 | $10,800 | (8,880) | $240 | 2,160 | 0.567 | 1,225 |

| 6 | $9,000 | ($7,740) | $240 | 1,500 | 0.507 | 761 |

| 7 | $7,200 | (6,600) | $240 | 840 | 0.452 | 380 |

| 8 | $5,400 | (5,460) | $240 | 180 | 0.404 | 73 |

| 9 | $3,600 | (4,320) | $240 | (480) | 0.361 | (173) |

| 10 | $1,800 | (3,180) | - | (1,380) | 0.322 | (444) |

| Net present value | $13,680 | |||||

Table (6)

Working Note (8):

Compute the amount of revenue:

| Year | Sales units | Selling price | Revenue | |

| (a) | (b) | (c) | ||

| 1 | $100,000 | $300 | 60% | $18,000 |

| 2 | $90,000 | $300 | 60% | $16,200 |

| 3 | $80,000 | $300 | 60% | $14,400 |

| 4 | $70,000 | $300 | 60% | $12,600 |

| 5 | $60,000 | $300 | 60% | $10,800 |

| 6 | $50,000 | $300 | 60% | $9,000 |

| 7 | $40,000 | $300 | 60% | $7,200 |

| 8 | $30,000 | $300 | 60% | $5,400 |

| 9 | $20,000 | $300 | 60% | $3,600 |

| 10 | $10,000 | $300 | 60% | $1,800 |

Table (7)

Working Note (9):

Compute the amount of expense:

| Year | Sales units | Total cost per unit | Purchase cost | Expense | |

| (a) | (b) | (c) | (c) | ||

| 1 | $100,000 | $190 | $3,400,000 | 60% | $(13,440,000) |

| 2 | $90,000 | $190 | $3,400,000 | 60% | $(12,300,000) |

| 3 | $80,000 | $190 | $3,400,000 | 60% | $(11,160,000) |

| 4 | $70,000 | $190 | $3,400,000 | 60% | $(10,020,000) |

| 5 | $60,000 | $190 | $3,400,000 | 60% | $(8,880,000) |

| 6 | $50,000 | $190 | $3,400,000 | 60% | $(7,740,000) |

| 7 | $40,000 | $190 | $3,400,000 | 60% | $(6,600,000) |

| 8 | $30,000 | $190 | $3,400,000 | 60% | $(5,460,000) |

| 9 | $20,000 | $190 | $3,400,000 | 60% | $(4,320,000) |

| 10 | $10,000 | $190 | $3,400,000 | 60% | $(3,180,000) |

Table (8)

4.

Ascertain the net present value for the given analysis; use the information in Requirement 3,

Explanation of Solution

Compute the salvage value for the new system:

Compute the net present value for the new system:

Thereby, the salvage value of the new system would increase the after-tax cash flows by $2,400,000. On the other hand, the NPV of the new system has been increased by $772,800, whereas, the NPV analysis for the old system remains unchanged. Thus this makes the new investment more attractive.

5.

Interpret the significance of providing accurate inputs for evaluating investments in automated manufacturing systems.

Explanation of Solution

Interpret the significance of providing accurate inputs for evaluating investments in automated manufacturing systems:

The key importance is that the usage of correct discount rate. Under requirement 2, the usage of 20% discount rate made the automated alternative system look entirely unappealing. Thus when using the correct discount rate (12%), the automated system results in a larger NPV, even though it was less than the NPV of the old system. However, the projections of future revenues for the old system were overly optimistic. On the other hand, the old system was not able to produce the same level of quality as the new system could produce. Thus, by considering the correct discount rate, the new system dominated the old. Moreover, the addition of salvage value simply increased this dominance.

Want to see more full solutions like this?

Chapter 19 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Newmarge Products Inc. is evaluating a new design for one of its manufacturing processes. The new design will eliminate the production of a toxic solid residue. The initial cost of the system is estimated at 860,000 and includes computerized equipment, software, and installation. There is no expected salvage value. The new system has a useful life of 8 years and is projected to produce cash operating savings of 225,000 per year over the old system (reducing labor costs and costs of processing and disposing of toxic waste). The cost of capital is 16%. Required: 1. Compute the NPV of the new system. 2. One year after implementation, the internal audit staff noted the following about the new system: (1) the cost of acquiring the system was 60,000 more than expected due to higher installation costs, and (2) the annual cost savings were 20,000 less than expected because more labor cost was needed than anticipated. Using the changes in expected costs and benefits, compute the NPV as if this information had been available one year ago. Did the company make the right decision? 3. CONCEPTUAL CONNECTION Upon reporting the results mentioned in the postaudit, the marketing manager responded in a memo to the internal audit department indicating that cash inflows also had increased by a net of 60,000 per year because of increased purchases by environmentally sensitive customers. Describe the effect that this has on the analysis in Requirement 2. 4. CONCEPTUAL CONNECTION Why is a postaudit beneficial to a firm?arrow_forwardBasuras Waste Disposal Company has a long-term contract with several large cities to collect garbage and trash from residential customers. To facilitate the collection, Basuras places a large plastic container with each household. Because of wear and tear, growth, and other factors, Basuras places about 200,000 new containers each year (about 20% of the total households). Several years ago, Basuras decided to manufacture its own containers as a cost-saving measure. A strategically located plant involved in this type of manufacturing was acquired. To help ensure cost efficiency, a standard cost system was installed in the plant. The following standards have been established for the products variable inputs: During the first week in January, Basuras had the following actual results: The purchasing agent located a new source of slightly higher-quality plastic, and this material was used during the first week in January. Also, a new manufacturing process was implemented on a trial basis. The new process required a slightly higher level of skilled labor. The higher- quality material has no effect on labor utilization. However, the new manufacturing process was expected to reduce materials usage by 0.25 pound per container. Required: 1. CONCEPTUAL CONNECTION Compute the materials price and usage variances. Assume that the 0.25 pound per container reduction of materials occurred as expected and that the remaining effects are all attributable to the higher-quality material. Would you recommend that the purchasing agent continue to buy this quality, or should the usual quality be purchased? Assume that the quality of the end product is not affected significantly. 2. CONCEPTUAL CONNECTION Compute the labor rate and efficiency variances. Assuming that the labor variances are attributable to the new manufacturing process, should it be continued or discontinued? In answering, consider the new processs materials reduction effect as well. Explain. 3. CONCEPTUAL CONNECTION Refer to Requirement 2. Suppose that the industrial engineer argued that the new process should not be evaluated after only one week. His reasoning was that it would take at least a week for the workers to become efficient with the new approach. Suppose that the production is the same the second week and that the actual labor hours were 9,000 and the labor cost was 99,000. Should the new process be adopted? Assume the variances are attributable to the new process. Assuming production of 6,000 units per week, what would be the projected annual savings? (Include the materials reduction effect.)arrow_forwardAustins cell phone manufacturer wants to upgrade their product mix to encompass an exciting new feature on their cell phone. This would require a new high-tech machine. You are excited about his new project and are recommending the purchase to your board of directors. Here is the information you have compiled in order to complete this recommendation: According to the information, the project will last 10 years and require an initial investment of $800,000, depreciated with straight-line over the life of the project until the final value is zero. The firms tax rate is 30% and the required rate of return is 12%. You believe that the variable cost and sales volume may be as much as 10% higher or lower than the initial estimate. Your boss understands the risks but asks you to explain the alternatives in a brief memo to the board, Write a memo to the Board of Directors objectively weighing out the pros and cons of this project and make your recommendation(s).arrow_forward

- Nico Parts, Inc., produces electronic products with short life cycles (of less than two years). Development has to be rapid, and the profitability of the products is tied strongly to the ability to find designs that will keep production and logistics costs low. Recently, management has also decided that post-purchase costs are important in design decisions. Last month, a proposal for a new product was presented to management. The total market was projected at 200,000 units (for the two-year period). The proposed selling price was 130 per unit. At this price, market share was expected to be 25 percent. The manufacturing and logistics costs were estimated to be 120 per unit. Upon reviewing the projected figures, Brian Metcalf, president of Nico, called in his chief design engineer, Mark Williams, and his marketing manager, Cathy McCourt. The following conversation was recorded: BRIAN: Mark, as you know, we agreed that a profit of 15 per unit is needed for this new product. Also, as I look at the projected market share, 25 percent isnt acceptable. Total profits need to be increased. Cathy, what suggestions do you have? CATHY: Simple. Decrease the selling price to 125 and we expand our market share to 35 percent. To increase total profits, however, we need some cost reductions as well. BRIAN: Youre right. However, keep in mind that I do not want to earn a profit that is less than 15 per unit. MARK: Does that 15 per unit factor in preproduction costs? You know we have already spent 100,000 on developing this product. To lower costs will require more expenditure on development. BRIAN: Good point. No, the projected cost of 120 does not include the 100,000 we have already spent. I do want a design that will provide a 15-per-unit profit, including consideration of preproduction costs. CATHY: I might mention that post-purchase costs are important as well. The current design will impose about 10 per unit for using, maintaining, and disposing our product. Thats about the same as our competitors. If we can reduce that cost to about 5 per unit by designing a better product, we could probably capture about 50 percent of the market. I have just completed a marketing survey at Marks request and have found out that the current design has two features not valued by potential customers. These two features have a projected cost of 6 per unit. However, the price consumers are willing to pay for the product is the same with or without the features. Required: 1. Calculate the target cost associated with the initial 25 percent market share. Does the initial design meet this target? Now calculate the total life-cycle profit that the current (initial) design offers (including preproduction costs). 2. Assume that the two features that are apparently not valued by consumers will be eliminated. Also assume that the selling price is lowered to 125. a. Calculate the target cost for the 125 price and 35 percent market share. b. How much more cost reduction is needed? c. What are the total life-cycle profits now projected for the new product? d. Describe the three general approaches that Nico can take to reduce the projected cost to this new target. Of the three approaches, which is likely to produce the most reduction? 3. Suppose that the Engineering Department has two new designs: Design A and Design B. Both designs eliminate the two nonvalued features. Both designs also reduce production and logistics costs by an additional 8 per unit. Design A, however, leaves post-purchase costs at 10 per unit, while Design B reduces post-purchase costs to 4 per unit. Developing and testing Design A costs an additional 150,000, while Design B costs an additional 300,000. Assuming a price of 125, calculate the total life-cycle profits under each design. Which would you choose? Explain. What if the design you chose cost an additional 500,000 instead of 150,000 or 300,000? Would this have changed your decision? 4. Refer to Requirement 3. For every extra dollar spent on preproduction activities, how much benefit was generated? What does this say about the importance of knowing the linkages between preproduction activities and later activities?arrow_forwardJonfran Company manufactures three different models of paper shredders including the waste container, which serves as the base. While the shredder heads are different for all three models, the waste container is the same. The number of waste containers that Jonfran will need during the following years is estimated as follows: The equipment used to manufacture the waste container must be replaced because it is broken and cannot be repaired. The new equipment would have a purchase price of 945,000 with terms of 2/10, n/30; the companys policy is to take all purchase discounts. The freight on the equipment would be 11,000, and installation costs would total 22,900. The equipment would be purchased in December 20x4 and placed into service on January 1, 20x5. It would have a five-year economic life and would be treated as three-year property under MACRS. This equipment is expected to have a salvage value of 12,000 at the end of its economic life in 20x9. The new equipment would be more efficient than the old equipment, resulting in a 25 percent reduction in both direct materials and variable overhead. The savings in direct materials would result in an additional one-time decrease in working capital requirements of 2,500, resulting from a reduction in direct material inventories. This working capital reduction would be recognized at the time of equipment acquisition. The old equipment is fully depreciated and is not included in the fixed overhead. The old equipment from the plant can be sold for a salvage amount of 1,500. Rather than replace the equipment, one of Jonfrans production managers has suggested that the waste containers be purchased. One supplier has quoted a price of 27 per container. This price is 8 less than Jonfrans current manufacturing cost, which is as follows: Jonfran uses a plantwide fixed overhead rate in its operations. If the waste containers are purchased outside, the salary and benefits of one supervisor, included in fixed overhead at 45,000, would be eliminated. There would be no other changes in the other cash and noncash items included in fixed overhead except depreciation on the new equipment. Jonfran is subject to a 40 percent tax rate. Management assumes that all cash flows occur at the end of the year and uses a 12 percent after-tax discount rate. Required: 1. Prepare a schedule of cash flows for the make alternative. Calculate the NPV of the make alternative. 2. Prepare a schedule of cash flows for the buy alternative. Calculate the NPV of the buy alternative. 3. Which should Jonfran domake or buy the containers? What qualitative factors should be considered? (CMA adapted)arrow_forwardFriedman Company is considering installing a new IT system. The cost of the new system is estimated to be 2,250,000, but it would produce after-tax savings of 450,000 per year in labor costs. The estimated life of the new system is 10 years, with no salvage value expected. Intrigued by the possibility of saving 450,000 per year and having a more reliable information system, the president of Friedman has asked for an analysis of the projects economic viability. All capital projects are required to earn at least the firms cost of capital, which is 12 percent. Required: 1. Calculate the projects internal rate of return. Should the company acquire the new IT system? 2. Suppose that savings are less than claimed. Calculate the minimum annual cash savings that must be realized for the project to earn a rate equal to the firms cost of capital. Comment on the safety margin that exists, if any. 3. Suppose that the life of the IT system is overestimated by two years. Repeat Requirements 1 and 2 under this assumption. Comment on the usefulness of this information.arrow_forward

- Boxer Production, Inc., is in the process of considering a flexible manufacturing system that will help the company react more swiftly to customer needs. The controller, Mick Morrell, estimated that the system will have a 10-year life and a required return of 10% with a net present value of negative $500,000. Nevertheless, he acknowledges that he did not quantify the potential sales increases that might result from this improvement on the issue of on-time delivery, because it was too difficult to quantify. If there is a general agreement that qualitative factors may offer an additional net cash flow of $150,000 per year, how should Boxer proceed with this Investment?arrow_forwardGina Ripley, president of Dearing Company, is considering the purchase of a computer-aided manufacturing system. The annual net cash benefits and savings associated with the system are described as follows: The system will cost 9,000,000 and last 10 years. The companys cost of capital is 12 percent. Required: 1. Calculate the payback period for the system. Assume that the company has a policy of only accepting projects with a payback of five years or less. Would the system be acquired? 2. Calculate the NPV and IRR for the project. Should the system be purchasedeven if it does not meet the payback criterion? 3. The project manager reviewed the projected cash flows and pointed out that two items had been missed. First, the system would have a salvage value, net of any tax effects, of 1,000,000 at the end of 10 years. Second, the increased quality and delivery performance would allow the company to increase its market share by 20 percent. This would produce an additional annual net benefit of 300,000. Recalculate the payback period, NPV, and IRR given this new information. (For the IRR computation, initially ignore salvage value.) Does the decision change? Suppose that the salvage value is only half what is projected. Does this make a difference in the outcome? Does salvage value have any real bearing on the companys decision?arrow_forwardJavier Company has sales of 8 million and quality costs of 1,600,000. The company is embarking on a major quality improvement program. During the next three years, Javier intends to attack failure costs by increasing its appraisal and prevention costs. The right prevention activities will be selected, and appraisal costs will be reduced according to the results achieved. For the coming year, management is considering six specific activities: quality training, process control, product inspection, supplier evaluation, prototype testing, and redesign of two major products. To encourage managers to focus on reducing non-value-added quality costs and select the right activities, a bonus pool is established relating to reduction of quality costs. The bonus pool is equal to 10 percent of the total reduction in quality costs. Current quality costs and the costs of these six activities are given in the following table. Each activity is added sequentially so that its effect on the cost categories can be assessed. For example, after quality training is added, the control costs increase to 320,000, and the failure costs drop to 1,040,000. Even though the activities are presented sequentially, they are totally independent of each other. Thus, only beneficial activities need be selected. Required: 1. Identify the control activities that should be implemented, and calculate the total quality costs associated with this selection. Assume that an activity is selected only if it increases the bonus pool. 2. Given the activities selected in Requirement 1, calculate the following: a. The reduction in total quality costs b. The percentage distribution for control and failure costs c. The amount for this years bonus pool 3. Suppose that a quality engineer complained about the gainsharing incentive system. Basically, he argued that the bonus should be based only on reductions of failure and appraisal costs. In this way, investment in prevention activities would be encouraged, and eventually, failure and appraisal costs would be eliminated. After eliminating the non-value-added costs, focus could then be placed on the level of prevention costs. If this approach were adopted, what activities would be selected? Do you agree or disagree with this approach? Explain.arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College