Videos

(1)

Journalize the stock investment transactions in the books of Company SF.

(1)

Explanation of Solution

Trading securities: These are short-term investments in debt and equity securities with an intention of trading and earning profits due to changes in market prices.

Debit and credit rules:

- ■ Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - ■ Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the purchase of 5,000 shares of Company W, at $40 per share, and a brokerage commission of $500.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| March | 14 | Investments–Company W Stock | 200,500 | ||

| Cash | 200,500 | ||||

| (To record purchase of shares for cash) | |||||

Table (1)

- ■ Investments–Company W Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company W’s stock.

Prepare journal entry for the purchase of 1,800 shares of Company M, at $50 per share, and a brokerage commission of $198.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| April | 24 | Investments–Company M Stock | 90,198 | ||

| Cash | 90,198 | ||||

| (To record purchase of shares for cash) | |||||

Table (2)

- ■ Investments–Company M Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company M’s stock.

Prepare journal entry for sale of 2,600 shares of Company W, at $38, with a brokerage of $100.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 1 | Cash | 98,700 | ||

| Loss on Sale of Investments | 5,560 | ||||

| Investments–Company W Stock | 104,260 | ||||

| (To record sale of shares) | |||||

Table (3)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Loss on Sale of Investments is a loss or expense account. Since losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- ■ Investments–Company W Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

Prepare journal entry for the dividend received from Company W shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 30 | Cash | 840 | ||

| Dividend Revenue | 840 | ||||

| (To record receipt of dividend revenue) | |||||

Table (4)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company W’s stock.

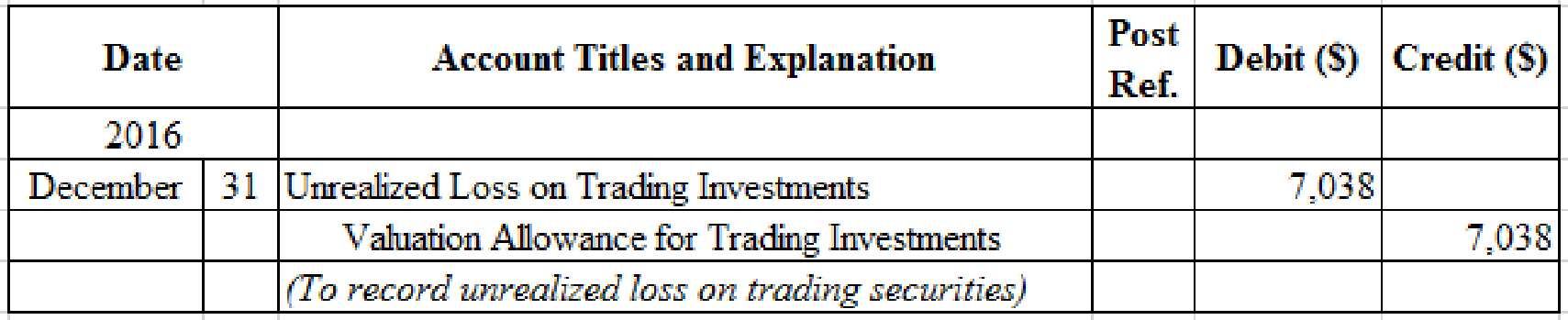

Prepare adjusting entry for valuation of trading securities transaction.

Figure (1)

- ■ Unrealized Loss on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses reduce stockholders’ equity value, and a decrease in stockholders’ equity value is debited.

- ■ Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was decreased (loss) to $179,400 from the cost of $136,438.

Working Notes:

Compute the unrealized gain (loss) as on December 31, 2016.

Step 1: Compute the fair value of the portfolio of the trading investment.

| Security | Number of Shares | Fair Market Value | = | Fair Market Value of Investment | |

| Company W | 2,400 shares | $38 | = | $91,200 | |

| Company M | 1,800 shares | 49 | = | 88,200 | |

| Total | $179,400 | ||||

Table (5)

Step 2: Compute the cost per share of Company W.

Step 3: Compute the cost per share of Company M.

Step 4: Compute the cost of the portfolio of the trading investment, as on December 31.

| Security | Number of Shares | Cost per Share | = | Cost of Investment | |

| Company W | 2,400 shares | $40.10 | = | $96,240 | |

| Company M | 1,800 shares | 50.11 | = | 90,198 | |

| Total | $186,438 | ||||

Table (6)

Note: Refer to Steps 3 and 4 for cost per share of Company W and Company M.

Step 5: Compute the unrealized gain (loss) as on December 31, 2016.

| Details | Amount ($) |

| Trading investments at fair value, December 31 (From Table-5) | $179,400 |

| Less: Trading investments at cost, December 31 (From Table-6) | (186,438) |

| Unrealized loss on trading investments | $(7,038) |

Table (7)

Prepare journal entry for the purchase of 3,500 shares of Company D, at $30 per share, and a brokerage commission of $175.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| April | 4 | Investments–Company D Stock | 105,715 | ||

| Cash | 105,715 | ||||

| (To record purchase of shares for cash) | |||||

Table (8)

- ■ Investments–Company D Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company D’s stock.

Prepare journal entry for the dividend received from Company W shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| June | 28 | Cash | 960 | ||

| Dividend Revenue | 960 | ||||

| (To record receipt of dividend revenue) | |||||

Table (9)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company W’s stock.

Prepare journal entry for sale of 700 shares of Company D at $32, with a brokerage of $50.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| September | 9 | Cash | 22,350 | ||

| Gain on Sale of Investments | 1,315 | ||||

| Investments–Company D Stock | 21,035 | ||||

| (To record sale of shares) | |||||

Table (10)

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Gain on Sale of Investments is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

- ■ Investments–Company D Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

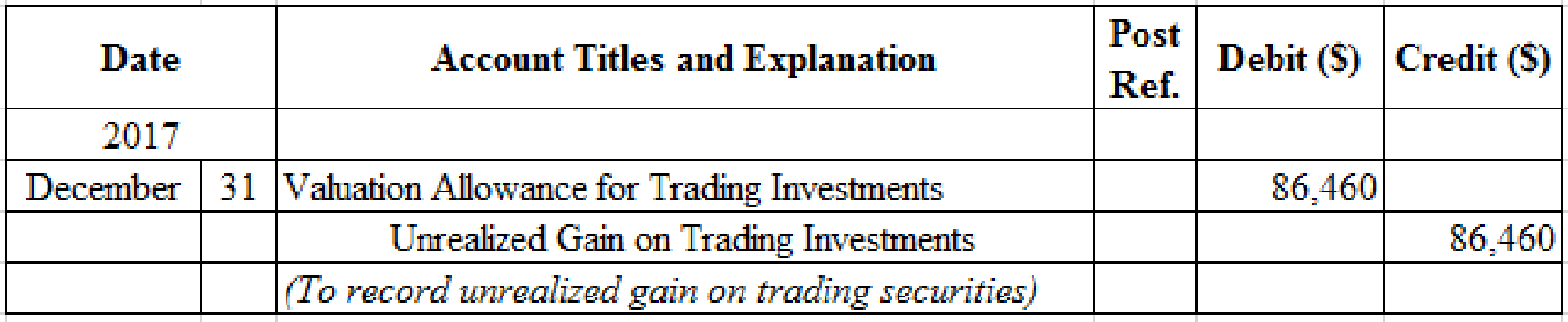

Prepare adjusting entry for valuation of trading securities transaction.

Figure (2)

- ■ Valuation Allowance for Trading Investments is a contra-asset account. The account is debited because the market price was increased (gain).

- ■ Unrealized Gain on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since gain has occurred and gains increase stockholders’ equity value, and an increase in stockholders’ equity value is credited.

Working Notes:

Compute the unrealized gain (loss) as on December 31, 2017.

| Details | Amount ($) |

| Unrealized gain as on December 31, 2017 | $79,422 |

| Add: Unrealized loss as on December 31, 2016 (From Table-8) | 7,038 |

| Unrealized gain on trading investments | $86,460 |

Table (11)

(2)

Indicate the presentation of trading investments on the current assets section of the balance sheet.

(2)

Explanation of Solution

Balance sheet presentation:

| Company S | ||

| Balance Sheet (Partial) | ||

| December 31, 2017 | ||

| Assets | ||

| Current assets: | ||

| Trading investments (at cost) | $270,578 | |

| Add valuation allowance for trading investments | 79,422 | |

| Trading investments (at fair value) | $350,000 | |

Table (12)

(3)

Discuss the reporting of trading investments on the financial statements.

(3)

Explanation of Solution

Unrealized gain or loss is the result of change in trading investments cost and fair values, and reported as Other Revenues (Losses) on the income statement. The unrealized gain will be added to the net income and unrealized loss will be deducted from the net income. In 2016, Company S would report $7,038 of unrealized loss as Other Losses on the income statement. In 2017, Company S would report $86,460 of unrealized gain as Other Income on the income statement.

Want to see more full solutions like this?

Chapter 15 Solutions

Financial Accounting

- Rantzow-Lear Company buys and sells debt securities expecting to earn profits on short-term differences in price, and holds these investments in its trading portfolio. The company’s fiscal year ends on December 31. The following selected transactions relating to Rantzow-Lear’s trading account occurred during December 2024 and the first week of 2025. December 17, 2024 Purchased 195 Grocers’ Supply Corporation bonds at par for $487,500. December 28, 2024 Received interest of $5,800 from the Grocers’ Supply Corporation bonds. December 31, 2024 Recorded any necessary adjusting entry relating to the Grocers’ Supply Corporation bonds. The market price of the bond was $3,000 per bond. January 5, 2025 Sold the Grocers' Supply Corporation bonds for $546,000. Prepare the appropriate journal entry or entries for each transaction. Indicate any amounts that Rantzow-Lear Company would report in its 2024 balance sheet and income statement as a result of this investment. Ignore income…arrow_forwardRantzow - Lear Company buys and sells debt securities expecting to earn profits on short-term differences in price, and holds these investments in its trading portfolio. The company's fiscal year ends on December 31. The following selected transactions relating to Rantzow - Lear's trading account occurred during December 2024 and the first week of 2025. December 17, 2024 Purchased 195 Grocers' Supply Corporation bonds at par for $487,500. December 28, 2024 Received interest of $5,800 from the Grocers' Supply Corporation bonds. December 31, 2024 Recorded any necessary adjusting entry relating to the Grocers' Supply Corporation bonds. The market price of the bond was $3,000 per bond. January 5, 2025 Sold the Grocers' Supply Corporation bonds for $546,000. Required: Prepare the appropriate journal entry or entries for each transaction. Indicate any amounts that Rantzow - Lear Company would report in its 2024 balance sheet and income statement as a result of this investment. Ignore income…arrow_forwardOn July 1, 2016. Elm Company purchased cash eight P 1,000 , 9% bonds of Celebrity Corporation at P 100 plus accrued interest. The bond interest is paid semiannually each May 1 and November 1. The bond maturity date is November 1, 2017. Elm Company's annual reproting period ends December 31. Elm Company classifies this investment as trading security. At December 31, 2016 , Celebrity bonds were quoted at P 97. REQUIRED : a. Give tne entry for Elm Company to record the purchase of the bonds on July 1, 2016 b. Give the entry to record the interest collected during 2016.arrow_forward

- On April 1, 2017 the Reba Company purchased 10%, $800,000 bonds of the Trading Up Company at par plus accrued interest. These bonds were classified as an investment in trading securities. The bonds pay interest on June 30 and December 31 each year. The entry by Reba on April 1, 2017, would include a debit to Investment in Trading Securities of $820,000 debit to Interest Expense of $20,000 credit to Interest Income of $20,000 credit to Cash of $820,000arrow_forwardOn January 1, 2017, KLM Company purchased bonds with faceamount of 5,000,000. The entity paid 4,600,000 plus transaction cost of 142,290. The bonds mature on December 31, 2019 and pay 6% interest annually on December 31 of each year with 8% effective yield. The bonds were quoted at 106.5 on December 31, 2017 and 108 on December 31, 2018. Assume that the business model in managing financial asset is to collect contractual cash flows that are solely for payment of principal and interest and also to sell the bonds in an open market. What is the balance of unrealized gain-OCI on December 31, 2017?arrow_forwardJourn Co. purchased short-term investments in available-for-sale debt securities at a cost of $51,700 cash on November 25. At December 31, these securities had a fair value of $50,400. This is the first and only time the company has purchased such securities. 1. 2. & 3. Prepare the November 25 entry to record the purchase of debt securities, the December 31 year-end adjusting entry for the securities' portfolio, and the April 6 entry when Journ sells 11% of these securities ($5,687 cost) for $6,700 cash. Record purchase of available-for-sale securities. Date General Journal Debit Credit Nov. 25 Record the year-end adjustment to fair value, if any. Note: Enter debits before credits. Date General Journal Debit Credit Dec. 31 Record sale of 11% of available-for-sale securities. Note: Enter debits before…arrow_forward

- Debt investment transactions, available-for-sale valuationRios Co. is a regional insurance company that began operations on January 1, 2021. The following selected transactions relate to investments acquired by Rios Co., which has a fiscal year ending on December 31:2021Feb. 1 Purchased 7,500 shares of Caldwell, Inc. common stock at $50 per share plus a brokerage commission of $75. Caldwell has 100,000 shares of common stock outstanding.May 1 Purchased securities of Holland, Inc. as a trading investment for $126,000.July 1 Sold 4,500 shares of Caldwell, Inc. for $46 per share less a $110 brokerage commission.July 31 Received an annual dividend of $0.50 per share on 3,000 shares of Caldwell, Inc. stock.Nov. 15 Sold the remaining shares of Caldwell, Inc. for $51 per share less a $90 brokerage commission.Dec. 31 The trading securities of Holland, Inc. have a fair value on December 31 for $120,000. 2022 Apr. 1 Purchased securities of Fuller, Inc. as a trading investment for $125,000. Oct.…arrow_forwardRantzow-Lear Company buys and sells debt securities expecting to earn profits on short-term differences in price, and holds these investments in its trading portfolio. The company's fiscal year ends on December 31. The following selected transactions relating to Rantzow-Lear's trading account occurred during December 2024 and the first week of 2025. December 17, 2024 Purchased 100 Grocers' Supply Corporation bonds at par for $350,000. December 28, 2024 Received interest of $2,000 from the Grocers' Supply Corporation bonds. December 31, 2024 Recorded any necessary adjusting entry relating to the Grocers' Supply Corporation bonds. The market price of the bond was $4,000 per bond. January 5, 2025 Sold the Grocers' Supply Corporation bonds for $395,000. Required: 1. Prepare the appropriate journal entry or entries for each transaction. 2. Indicate any amounts that Rantzow-Lear Company would report in its 2024 balance sheet and income statement as a result of this investment. Ignore income…arrow_forwardStave Company invests $10,000,000 in 5% fixed rate corporate bonds on January 1, 2017. All the bonds are classified as available-for-sale and are purchased at par. At year-end, market interest rates have declined, and the fair value of the bonds is now $10,600,000. Interest is paid on January 1. Prepare journal entries for Stave Company to (a) record the transactionsrelated to these bonds in 2017, assuming Stave does not elect the fair option; and (b) record the transactions related to these bonds in 2017, assuming that Stave Company elects the fair value option to account for these bonds.arrow_forward

- Journ Co. purchased short-term investments in available-for-sale debt securities at a cost of $50,000 cash on November 25. At December 31, these securities had a fair value of $47,000. This is the first and only time the company has purchased such securities. 1. Prepare the November 25 entry to record the purchase of debt securities. 2. Prepare the December 31 year-end adjusting entry for the securities’ portfolio. 3. Prepare the April 6 entry when Journ sells 10% of these securities ($5,000 cost) for $6,000 cash.arrow_forwardOn January 1, 2017, Henderson Corporation redeemed $500,000 of bonds at 99. At the time of redemption, the unamortized premium was $15,000. Prepare the corporation’s journal entry to record the reacquisition of the bonds .arrow_forwardWeaver Company has the following data at December 31, 2015 for its securities: Securities COST FAIR VALUE Debt Investments - Trading 90,000 87,000 Debt Investments - Available for sale 74,000 75,000 Stock Investments 80,000 76,000 Prepare the adjusting entries to report the securities at fair value. On what financial statement and in what section of that statement would each of the above accounts be reported. (6 all together) a Date Account Title Debit Creditarrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning